TRADERUN

MOODUL TRADERUN

MODULE BUSINESS PECULIARITIES IN THE EU,

RUSSIA AND

EASTERN PARTNERSHIP COUNTRIES

ÄRI ERIPÄRAD EUROOPA LIIDUS, VENEMAAL JA IDAPARTNERLUSRIIKIDES

Lecturers: Ryhor Nizhnikau (

responsible ) Giorgi Gaganidze,

Sergei Proskura, Andres Assor

P2EC.00.202 (UT

code ), RIE 7044 (TLU code)

Reading materials: Business peculiarities in

Ukraine and

Belarus Lugemismatejal: Äri eripärad Ukrainas ja Valgenenes

Created by Andres Assor Tartu 2013

TABLE OF CONTENTS

INTRODUCTION ................................................................................................................... 4

1.

UKRAINE ...................................................................................................................... 5

1.1.

General information ..................................................................................................... 5

1.1.1. Country Profile ..................................................................................................... 5

1.1.2. Post-Independent Ukraine. Economy and politics ............................................... 6

1.1.3. Key Macroeconomic indicators ......................................................................... 14

1.1.4. Foreign Direct Investments ................................................................................ 16

1.1.5. Demographics and labor force .......................................................................... 17

1.1.6. New emerging industry ....................................................................................... 19

1.2.

The Business Environment ........................................................................................ 23

1.3.

Banking system.......................................................................................................... 27

1.4.

Starting a business in Ukraine ................................................................................... 32

1.5.

Market entry strategies .............................................................................................. 33

1.5.1. Direct Sales ........................................................................................................ 33

1.5.2. Agency and Commission arrangements ............................................................. 34

1.5.3. Joint venture with a Ukrainian partner .............................................................. 34

1.5.4. Representative office (commercial and non-commercial) ................................. 34

1.5.5. Ukrainian subsidiary .......................................................................................... 35

1.6.

Foreign investment treatment .................................................................................... 35

1.7.

Corporate forms ......................................................................................................... 37

1.8.

Taxation ..................................................................................................................... 39

1.8.1. Corporate income tax (CIT) ............................................................................... 39

1.8.2. Withholding Tax (WHT) ..................................................................................... 41

1.8.3. Value Added Tax (VAT) ...................................................................................... 42

1.8.4. Transfer Pricing (TP) ......................................................................................... 43

1.8.5. Personal taxation ............................................................................................... 44

1.9.

Financial Reporting ................................................................................................... 45

1.10.

Currency regulations .............................................................................................. 46

1.11.

Risk of UAH devaluation ....................................................................................... 48

2.

BELARUS .....................................................................................................................51

2.1.

General information ................................................................................................... 51

2.1.1. Country Profile ................................................................................................... 51

2.1.2. Overview of Belarusian economy ....................................................................... 52

2.2.

Customs Union of Belarus,

Russia and Kazakhstan.................................................. 55

2.3.

The Business Environment ........................................................................................ 58

2.4.

Banking system.......................................................................................................... 59

2.5.

Development of Private

Sector .................................................................................. 61

2.5.1. Starting a business in Belarus ............................................................................ 63

2.6.

Foreign Investment treatment .................................................................................... 66

2.7.

Corporate forms ......................................................................................................... 71

2.7.1. Limited Liability Company ................................................................................. 72

2.7.2. Joint- Stock Company .......................................................................................... 73

2.7.3. Private unitary enterprise .................................................................................. 74

2.7.4. Registration of the companies in Belarus .......................................................... 75

2.8.

Taxation ..................................................................................................................... 75

2.8.1. Corporate income tax (CIT) ............................................................................... 75

2.8.2. Withholding tax (WHT) ...................................................................................... 78

2

2.8.3. Value Added Tax (VAT) ...................................................................................... 80

2.8.4. Transfer Pricing (TP) ......................................................................................... 82

2.8.5. Personal Taxation .............................................................................................. 82

2.9.

Financial Reporting ................................................................................................... 83

2.10.

Currency Regulations ............................................................................................. 86

Appendix 1. Ukraine. Key macroeconomic

forecasts . ...........................................................89

Appendix 2. Ukraine. Development of IT

Outsourcing industry - selected charts ..................90

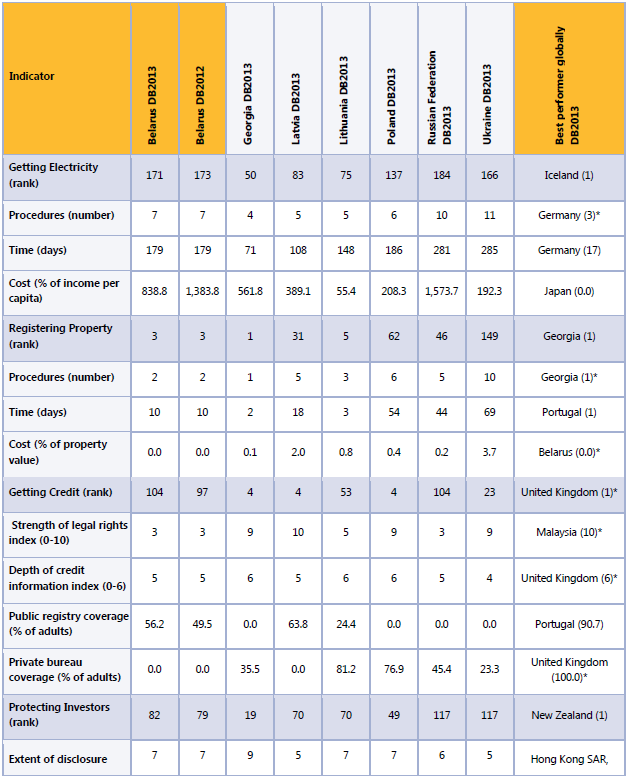

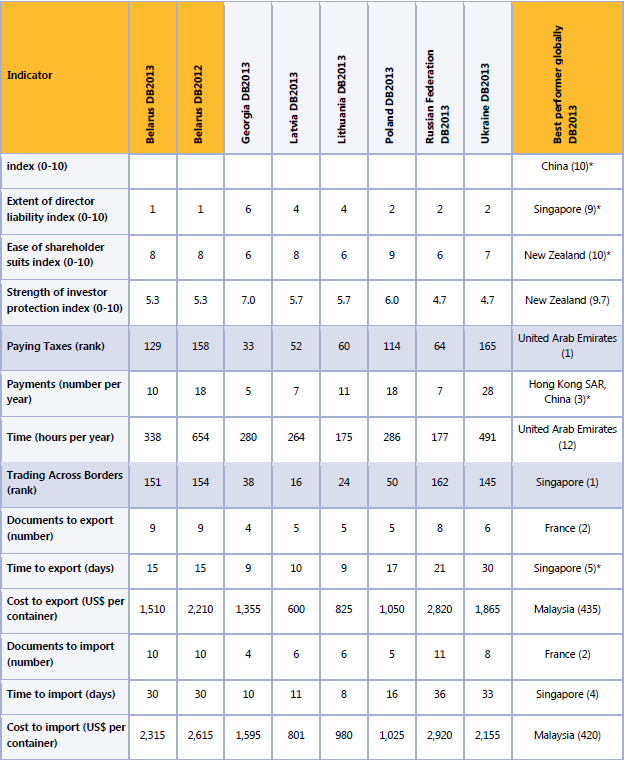

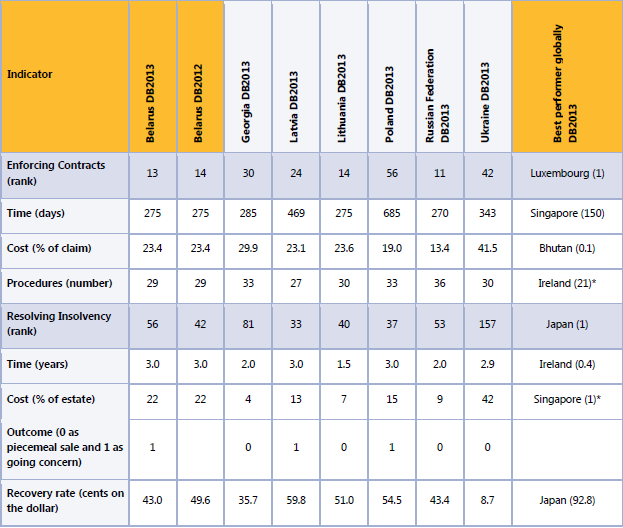

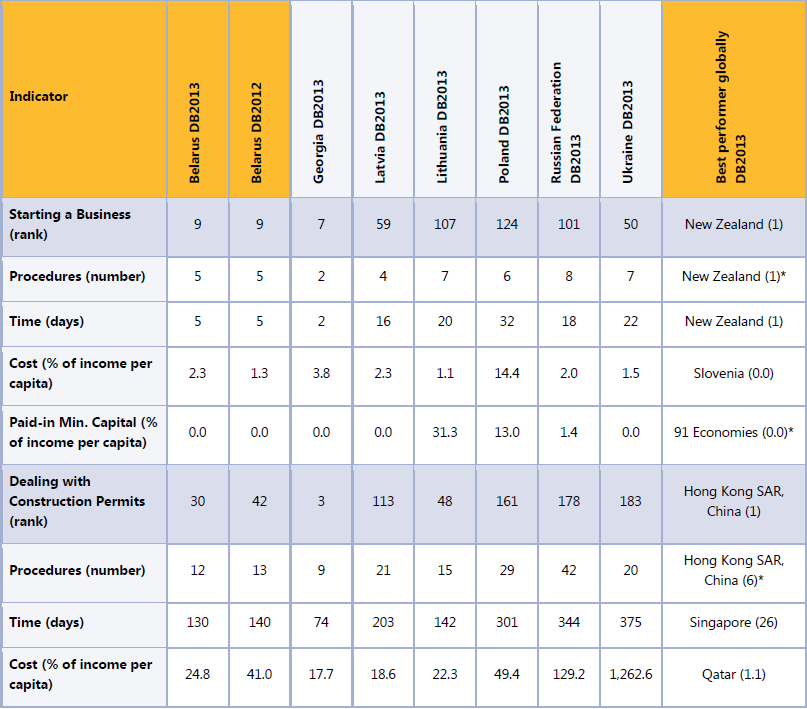

Appendix 3. Ukraine. Summary of Doing Business indicators...............................................92

Appendix 4. Ukraine.

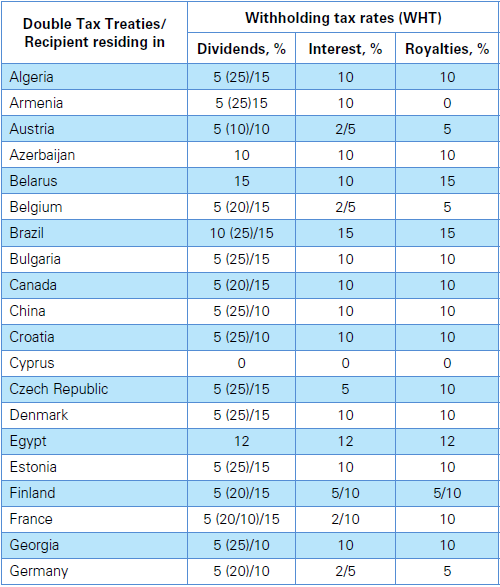

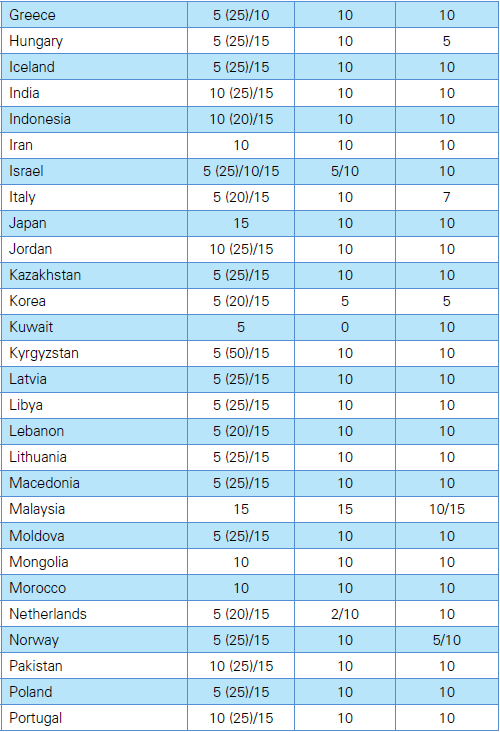

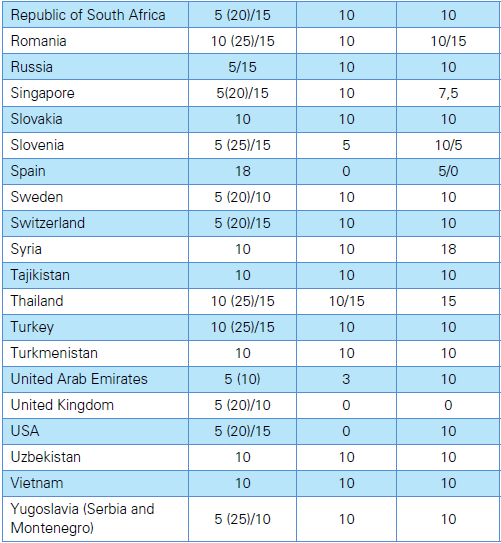

Chart of withholding tax rates. ............................................................96

Appendix 5. Belarus. Summary of Doing Business indicators. ..............................................99

Appendix 6. Belarus. Chart of withholding tax rates. ........................................................... 103

References ......................................................................................................................... 104

ABOUT TRADERUN

PROGRAMME .................................................................................. 106

3

INTRODUCTION The

current reading

material focuses on business peculiarities in Ukraine and Belarus.

***

The aim of the Traderun programme course “FUNDING PROJECTS IN RUSSIA AND EASTERN

PARTNERSHIP COUNTRIES” is to provide the students with comprehensive and practical

overview of the fundraising possibilities in EU and Estonia. The course gives an overview of

EU structural support and regional implementing agencies, that are available for a

businessman to apply for a fund.

A successful student will be aware of and understand the EU fundraising possibilities in the

frames of cooperation with Russian and Eastern Partnership countries, and able to define the

financing criteria and priorities.

The current reading material summarises the main aspects covered by lectures and

structurises the information channels for the future.

The course supports the other Traderun courses, especially the course related to EU

cooperation with Russia and Eastern Partnership Countries.

4

1. UKRAINE 1.1. General information 1.1.1. Country Profile

Capital: Kyiv.

Total area: 603,550 sq. km (the largest country in

Europe by area that is physically

within Europe entirely).

Population: ~ 45 million (

declining).

Major cities and

estimated population (

Good news

! Not all the business and capital concentrated in the capital):

Kyiv (

Kiev ) – 2.8 million,

Kharkiv (Kharkov) – 1.5 million,

Lviv (

Lvov ) - 1.5 million,

Donetsk – 1 million,

Dnipropetrovsk (Dnepropetrovsk) - 1 million,

Odesa (Odessa) – 1 million.

Zaporizhzhya (Zaporozhye) – 0.8 million.

5

GDP

growth , %: 1.0 (2013

forecast EBRD – downward revision from previously projected

2.5%).

Official language : Ukrainian (

although Russian is widely used in business

communication ).

Currency: Hryvnya (UAH).

Government type:

republic .

Membership: the United Nations, the International Monetary Fund (IMF), the World

Bank , the European Bank for

Reconstruction and Development (EBRD), the World Trade

Organization (WTO), etc.

Ukraine is bordered by Russia in the

east , the

Black Sea in the

south ,

Moldova , Romania,

Hungary,

Slovakia and

Poland in the

west , and Belarus in the

north . The country is

rich in

mineral resources:

iron ore,

coal , manganese, natural gas (

shale – costly and dangerous to

extract), oil,

sulfur , graphite,

titanium , magnesium, kaolin, nickel,

mercury , timber and

others .

It’s commonly

known that Ukraine is politically

divided between its

Western and Eastern

regions . Ukraine's geography and history have played an

important role in the country's

current

political crisis . Western parts of the country at

times belonged to Poland, Austro-

Hungary, and Czechoslovakia,

while eastern and

southern parts belonged to Russian

Empire .

Only after World War II did Ukraine attain its

present borders as a republic within the

Soviet Union. That history

partly explains Ukraine's voting

patterns , political sympathies, and

outlook on the future.

Population of Western Ukraine largely supports politics paying EU card (Yusteshenko,

Tymoshenko), while

industrial Eastern regions support Yanukovych as Politian closely

associated with better relation / integration with Russia.

1.1.2. Post-Independent Ukraine. Economy and politics

1990-s

When Ukraine

became independent in 1991,

there were

expectations that it would in the

near future become a wealthy free market

democracy and a

full member of the European

and Euro-

Atlantic communities. Ukraine

never fulfilled those expectations. Instead, it is

seen as an underachiever, sometimes as a sick man of Europe, and

perhaps even as a potentially

failed state thanks to its geopolitical situation, historical burdens, and the mistakes made in

institutional development and

policy .

Economically, Ukraine has

grown along with the

region . As

such , growth rates have not been

low, but they

come after the economically devastating

1990s and are not

built on a

6

sustainable foundation. For

years Russia

provided Ukraine with underpriced gas while

Ukraine’s

export prices increased rapidly. Over the decades Ukraine,

however , grew

dependent on oil and gas

coming from Russia, at

almost no

cost .

Today , 70

percent of gas

consumed in the country is imported.

In 1991 Ukraine was one of the poorest Soviet republics. Statistics for the time are

notoriously uncertain, but the

best ones available show Ukraine’s GDP at just $1,307 per

capita . Only

Azerbaijan ,

Georgia , Kyrgyzstan, Tajikistan, and Uzbekistan lagged

behind Ukraine; even Moldova and Turkmenistan, generally regarded as very

poor Soviet republics,

were

ahead of Ukraine.

Ukraine’s economy contracted annually between 9.7 and 22.7 percent in 1991–1996. The

country experienced hyperinflation and an exceptionally huge

production decline for a

country not ravaged by a major war. Official GDP collapsed by almost

half from 1990 to

1994, and

slow decline continued throughout the decade.

Economic growth would not

resume again until 2000. The

budget deficit was, at 14.4 percent of GDP, exceptionally large.

Barter and the use of surrogate moneys and foreign currencies

prevailed . Ukraine had

introduced a sovereign currency, the Hryvnia, but it was

little used. A

shadow economy

swelled and compensated for an unknown

share of the economic collapse.

2001-2008

Between 2001 and 2008, the Ukrainian economy picked up significantly. Many of Ukraine’s

large-

scale capitalists—the oligarchs—are

former Soviet-era industrial managers who

succeeded on a grand scale when industries were privatized. Their

wealth was originally

based on a

traditional ,

simple formula :

convert cheap energy and raw materials into

metals and manufactured

goods . The six richest Ukrainians are all metallurgy magnates.

In Ukraine—like in Russia—incumbent managers (

there is a special term in Russian for such

executives/ owners – Red Director ) were present at the

birth of private property and

could harness privatization. The political atmosphere of

nation building helped

keep foreigners —

Russians and Westerners alike—mostly out of the

game . The major exception was the

financial system;

several banks both from the West and the East have entered Ukrainian

markets .

Crucially for Ukraine’s survival, between 2001 and 2008, as metals and

chemicals prices

boomed on the

back of

fast international economic growth while the

price of gas imported

from Russia remained low,

terms of trade

improved by 50 percent. Monetization also helped

to drive this boom, as the

ratio of

credit to GDP grew extremely fast—from 7 to almost 80

percent over just several years.

7

In less

than a decade, Ukraine leaped from an economy not based on

money to

having a

banking sector comparable in relative

size to that of many well-

established market

economies . Credit was at last available, and not only from state-controlled and other

politically connected banks, but from reputable foreign banks channeling

easy international

liquidity to Ukraine as they did to other emerging economies.

From 2000 to 2007, Ukraine’s

real growth averaged 7.4 percent and was thus very

similar to

Russia’s. In both countries, this growth was driven by

domestic demand : orientation

toward consumption , other structural

change , and financial development. In Ukraine, domestic

demand grew in

constant prices by almost 15 percent annually. It was supported by

expansionary—pro-cyclical—fiscal policy generally driven by populism for

perceived short-

term political

gain .

Further , industrial

capacity left idle in the 1990s was

brought into use, capital inflows surged

after 2005, and credit growth was fueled by

external borrowing. In terms of markets, in

2000, the EU was

already the largest, purchasing almost a third of Ukraine’s exports. It was

followed by Russia and

Asia , with a share of just under a

quarter for both. In 2009, Asia

passed the EU, but together they

still accounted for 55 percent of exports. Fast-

growing Asian economies are now the

basic consumers of Ukrainian metallurgy

products , and

Russia’s exports of oil and gas suffer from low growth in Europe more than Ukraine’s exports

do.

Meanwhile , the price of gas remained low. In 2008, the price

paid by Ukraine for gas was still

less than half of that paid by Western European countries. Over a longer

period , this growth

pattern was

bound to be unsustainable. This is the most important

single fact of Ukraine’s

economic prospects. The improving terms of trade of the 2000s were a

positive windfall, but

Ukraine did not

know how to use that windfall wisely. Ukraine’s economy and its growth

prospects ultimately suffered from its nationalism and inefficiency.

The windfall Ukraine enjoyed meant that industry did not have to diversify or become more

sophisticated—two

characteristics that are

necessary for

competition in today’s markets. In

2000, metals and mineral products accounted for half of Ukraine’s exports.

Adding agro-food

and chemicals

took the

proportion to just over 70 percent. In 2008, the

shares remained

quite similar, with agro-food increasing from 11 to 16 percent.

Steel export

unit value grew

more than

four times between 2000 and 2008, while steel export

volume grew only little

between 2000 and 2004, and then stagnated.

Missteps in Domestic Economy

With a windfall to rely on, Ukraine not only failed to diversify its exports but also

mismanaged its domestic economy.

Since 1992 Ukraine has had just one

year , 2002, with a

8

balanced budget. Income growth has been huge, and the ratio of domestic savings declined

as consumption boomed. Since 2001 annual growth in

average monthly earnings has always

surpassed

consumer price inflation, until 2008 quite frequently by more than 20 percentage

points and never much

below that. Such income growth was supported by the country’s high

export, especially steel, prices.

Boosted by rapidly improving terms of trade,

import volumes grew much faster than export

volumes and the net growth impact of foreign trade was

negative by some 5 percent

annually. As imports were liberalized in the 1990s, consumers and investors alike

preferred the

superior quality ,

choice , and

brands available from world markets. By the 2000s an

increasing share of

them could afford foreign goods. Cheap imports from Asian and other

countries also became available. The trade

balance has been consistently negative since

2005, and the current

account has followed since 2006.

Imports contribute to

welfare , but for that to be sustainable, any country also has to be able

to

cover the import bill with exports,

running down reserves, inward investment (direct or

other), or raising foreign credit. But exports, of course, were not

providing the necessary

boost. And Ukraine had to

begin with in

practice no official reserves or foreign

assets and

liabilities, as Russia had taken responsibility for the Soviet bequest. Ukraine inherited no

assets to run down. And no

reserve funds were built to

sustain the fiscal situation over a

longer term. Thus, Ukraine’s dependence on foreign,

usually short-term, funding increased

(which would

prove dangerous in the 2008 crisis and will threaten Ukraine in the future as

well).

Net inward foreign direct investment (FDI) has been positive since 1992, varying in 2005–

2010 between $5 and $10

billion annually. But most foreign direct investment has

gone to

closed-sector

services such as retail trade and

finance , while the industries inherited from

the Soviet Union were privatized to domestic owners and are controlled by oligarchs.

These industries have

typically failed to become more

competitive in more than a decade. Major

needs for infrastructure investment have accumulated.

In

contrast to traditional industries, foreign entry into financial services was encouraged. Up

to 40 percent of bank assets have been controlled by foreign entities, but the share is now

declining with only Russian banks penetrating the market. Some Western banks are

downsizing their

activities , and a few at

least wish to

exit , if they only could

without losing

their past investments.

In spite of inevitably worsening demographics, a huge

pension burden was created. In a

nation of 46 million inhabitants, the pensions of 14 million pensioners grew from 9.2 percent

of GDP in 2003 to almost 18 percent in 2009. This is one of the heaviest pension burdens

9

globally, and negative demographics will

continue to worsen the situation if needed

measures , like increasing the general pension age, are not taken.

The end of cheap gas

By the mid-2000s, Russia had reached several conclusions on energy and money that

started to rock Ukraine’s

position . The much-needed energy efficiency demanded a huge change in

the

whole of economy and society—as in Ukraine—a

process known in Russia as

modernization.

The

first necessary

condition for modernization was to

raise domestic gas and consequently

power prices. A roadmap for doing that was accepted in

late 2006, and an evident

conclusion emerged. If Russians had to pay more, there was no

reason why Belarusians,

Ukrainians, and others should continue to be subsidized.

The simple Russian

proposition has had dramatic consequences for Ukraine. Ukraine’s terms

of trade would change from a windfall to a downpour of cold rain. And Ukraine had not

made the necessary domestic reforms to

prepare for such a

turn of

events .

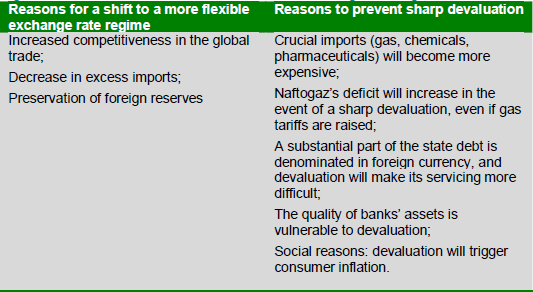

There have been aspiring political leaders who have thought that the Russian

decision may

be turned or at least postponed by playing on the Slavic or Eurasian Union cards: Ukrainians

will continue to entertain prospects of Eastern integration if Russia continues postponing

inevitable price hikes. Trying to

avoid the price

revolution is surely seen by some inside

Ukraine as a potent argument for

joining post-Soviet reintegration schemes, like Belarus has

done .

Others in Kiev

found virtue in necessity. In the end the price revolution would

benefit Ukraine by

making long-postponed reforms inevitable. Perhaps as well, excessive

dependence on Russia could be minimized by

developing domestic

sources of energy, like

unconventional gas. Others took solace in the possibility that Ukraine’s export prices might

in the end

increase faster than those of Russia’s exports.

Possibilities for the future have been explored, but meanwhile populist policies have

continued unabated. The Yanukovych government has refused to increase gas prices for

households, as demanded by the International Monetary Fund (IMF) as a key condition for

continued financial support.

Waste of energy by households thus continues unabated. There

has also been no progress in reducing the burden posed by excessive pension expenditures

on the budget—now and especially in the future.

Debt builds

10

Compounding this was the financial crisis that rocked the international economic system in

2007–2008. Ukraine’s

lack of sound domestic economic

structures and debt

accumulation made it especially difficult for the country to weather the financial storm. Gross reserves

have grown from less than a

month ’s imports to around

five months’ worth from 2005 to

2010, still a modest level. Public and private foreign debt has recently risen fast from more

than $10 billion in 1997–2002 to over $100 billion in 2008–2009. The 2008 level was 56.4

percent of GDP and 118.7 percent of exports.

In 2009, as GDP declined and the UAH weakened, external debt stock was 91.5 percent of

GDP and 191.6 percent of annual exports—

clearly an unsustainable level for Ukraine. In late

2011, Ukraine’s official reserves were some $30 billion. Paying back its debt—barring a

further accelerated depletion of foreign

exchange reserves—would be

close to impossible

without

fresh foreign finance, preferably in the form of disbursements from the IMF.

A two-year IMF

stand -by arrangement, put in

place in 2008, provided exceptional

access to

financing that was

crucial in helping Ukraine

through the Great Recession. In

particular , it

helped to

prevent a banking crisis. In many respects, however, Ukraine reneged on its

commitments, and the

program went off-

track very soon, as a 2011 IMF evaluation

concludes. This holds for fiscal, exchange

rate , and monetary policies, but in particular for

the energy sector.

In 2008, Ukraine committed itself to phasing out all gas subsidies in three years, but little

was done on that

front . For some

specific industries, gas prices were actually decreased in

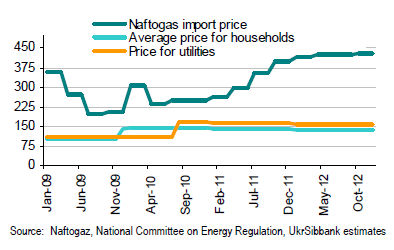

2009. Ukrainian households still pay traditionally extremely little for the gas their

everyday life depends on. At end of the year, gas prices for households accounted for about one-fifth

and those for

utilities for one-third of import prices. Officially the low gas prices are justified

as poverty alleviation, but it is difficult to imagine a less effective and less equitable pro-poor

policy.

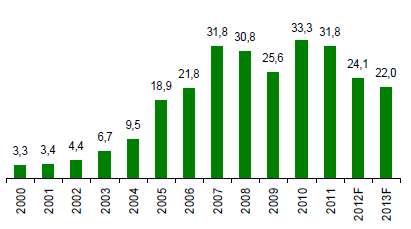

The chart below illustrates

dynamic of gas prices in Ukraine – import

vs household prices.

11

Source: Ukraine Macro Outlook for 2013 by UkrSibbank (BNP Paribas Group)

Following this, there was little left of Ukraine’s credibility as a policy program partner. Yet,

another stand-by arrangement amounting to $15.3 billion was somewhat surprisingly

approved by the IMF on

July 28, 2010.

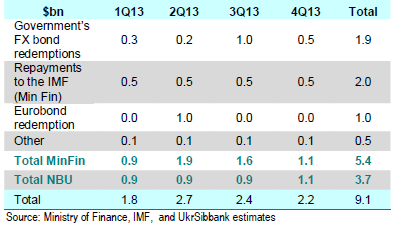

2013 is extremely challenging year for Ukraine in terms of servicing its debt. The table below

summarizes Ukraine’s FX (foreign currency) denominated debt repayment schedule for 2013

is billion $.

12

Source: Ukraine Macro Outlook for 2013 by UkrSibbank (BNP Paribas Group)

Not all bad news

Ukraine could be a rich country. No other European country can boast its resources of coal,

iron, gas, and rich agrarian

land . Almost three-quarters of its area is agricultural land, more

than half arable. Though the quality of legendary black earth deteriorated

during the Soviet

decades, it remains

among the best globally.

The country has some oil and conventional gas, and perhaps more importantly, possesses as

much as 4 percent of

global coal reserves. Though more than half of energy consumed is

imported, reserves of unconventional gas are estimated to be several trillions of cubic

meters in size, promising gas independence from Russia in about two decades. Indeed,

Ukraine’s growth rate in 2001–2008, boosted by exceptional improvement in terms of trade,

was fully comparable with Eurasian hydrocarbon

producers at some 7 percent annually.

Infrastructure is in spite of deterioration in relatively good

shape . The Soviet Union left

industries, for

instance in crucially important metallurgy, that are generally taken to be in

better condition than in Russia.

Ukraine was a potentially rich country made poor by a tragic history. During the years

following independence, Ukraine has grown with the region, but relative to many

expectations, this has been a bitter disappointment. Ukraine is seen as an underachiever.

Source: http://carnegieendowment.org/2012/03/09/underachiever-ukraine-s-economy -since-1991/a1nf# 13

1.1.3. Key Macroeconomic indicators For Key Macroeconomic indicators and forecasts

please refer to Appendix 1.

Ukraine’s economic sectors are

diverse , but in need of new capital and investments to

compete with sectors in the West. The country’s major export categories

include :

ferrous and non-ferrous metals,

steel products and steel structures;

chemical products (

including fertilizers;

plastics and

rubber );

agricultural products and food (mainly

grains , cereals; food

processing and packaging).

As seen from the list

above , Ukrainian economy is strongly dependent on various

commodities and as

result of price fluctuations of those commodities. Perhaps, the only

commodity group, which is in long-run

rather immune (not 100% though) to cyclical

changes are agricultural products.

Taking into account growing population

worldwide and gradual

income growth, particularly in food importing Asia and

Africa , it’s rather

safe assumption

that demand and prices for agricultural products will continue upwards trend. Ukraine with

Europe’s best and largest

areas for

agriculture is very well positioned to benefit from the

World’s growing demand for food.

Other commodities exported by Ukraine (such as steel, coal, chemicals etc) are and will

continue to be

affected by cycles of the global economy – there will be periods of growing

demand and prices hikes as well as periods of

slowing demand and declining price.

Ukraine’s dependence on energy supplies and the lack of significant structural reform have

made the Ukrainian economy vulnerable to external shocks. Ukraine depends on imports to

meet about 75% of its annual oil and natural gas

requirements and 100% of its

nuclear fuel

needs.

The

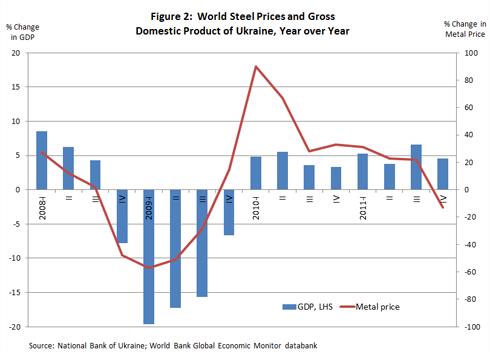

strong correlation between world commodity prices and Ukraine’s economic growth can

be seen in

Figure below.

14

A

drop in steel prices - Ukraine’s top export - and Ukraine’s exposure to the global financial

crisis because of

aggressive foreign borrowing lowered the GDP growth rate in 2008.

Ukraine reached an agreement with the IMF for a USD 16.4 billion Stand-By Arrangement in

November 2008 to deal with the economic crisis, but the program quickly stalled because

little progress was made in implementing reforms. The economy contracted

nearly 15% in

2009 - one of the worst economic performances in the world.

In April 2010, Ukraine negotiated a price discount on Russian gas imports in exchange for

extending Russia’s

lease on its

naval base in Crimea. In August 2010, Ukraine reached a new

agreement with the IMF for a USD 15.1 billion Stand-By Agreement to put the country on the

path to fiscal sustainability, reform the gas sector, and

shore up the country’s banking

system. Economic growth resumed in 2010 and 2011, buoyed by exports. After initial

disbursements, the IMF program stalled in

early 2011 due to the lack of progress in

implementing key gas sector reforms, namely gas tariff

increases (

obviously politically very

unpopular measure ).

Agriculture

fell to 9.3% of the total GDP in 2011 compared with 14% in 1999. Industry,

including

mining ,

manufacturing and

construction , continued to account for 34.7% in this

period. Meanwhile, trade and other services grew from 51 to 56.1 percent.

15

1.1.4. Foreign Direct Investments

Despite having huge potential, Ukrainian economy is critically lacking in foreign investments.

Percentage of FDI to GDP was declining very year since 2007 and, according to BNP Paribas

in Ukraine forecast, projected to continue declining during 2013-2104.

According to State Statistics

Service of Ukraine, foreign direct investment (FDI) in a form of

equity capital slowed substantially in 2012. FDI for the period of

January – September 2012

(3 quarters) amounted to USD 2.6 billion, which was 29.4% down year of a year.

Investments

came from 129 countries and regions. The ten largest

investor countries, which

account for over 82% of total FDI, are Cyprus with $15.076 billion in investment,

Germany with $7.4 billion, the

Netherlands with $5.04 billion, Russia with $3.71 billion, Austria with

$3.3 billion, the United Kingdom with $2.4 billion, the

British Virgin

Islands with $1.81 billion,

France with $1.8 billion,

Sweden with $1.58 billion, and Switzerland with $1.09 billion.

Industrial

enterprises received $16.866 billion in investment, which was 32% of total FID in

Ukraine. In particular, $13.936 billion was

invested in the processing industry $1.51 billion in

the production and distribution of electricity and gas, and the water

supply , and $1.424

billion in the mining industry.

In the processing industry the investment was

split in the following way: the

manufacture of

basic metals and fabricated metalware received $6.137 billion in direct investment, the

production of food,

beverages and tobacco got $2.995 billion, chemical and petrochemical

industry $1.321 billion,

engineering $1.156 billion, while the manufacture of other non-

metallic mineral products $1.013 billion.

Financial

institutions accumulated $15.702 billion in direct investment, which was 29.8% of

total

amount .

A total of $8.523 billion, or 16.2% of total FDI, was invested in

organizations that are

engaged in transactions with real

estate , rent and leasing, engineering, and services to

individuals, while $5.503 billion, or 10.4%, was invested in enterprises engaged in trade,

repairs of motor vehicles, household and personal goods.

Total foreign direct investment (equity and debt

instruments ) as of October 1, 2012 was

$6.252 billion.

The amount of direct investment (equity) from Ukraine in other countries as of October 1,

2012 was $6.428 billion, in particular, EU countries received $6.027 billion (93.7% of total

amount), the CIS countries $306 million (4.8%), and other countries $95 million (1.5%).

16

Direct investment from Ukraine went to 47 countries, the

lion ’s share

going to Cyprus

(90.4%). Total direct investment (equity and debt instruments) by Ukraine in other countries

as of October 1, 2012, amounted to $6.652 billion.

Source: The American Chamber of Commerce in Ukraine

The European Bank for Reconstruction and Development continues to be the largest

financial investor in Ukraine. As of January 1, 2013 the Bank has committed more than EUR

8.2 billion (USD 10.7 billion) in 318 projects. In 2012, the EBRD has invested EUR 934

million (USD 1.2 billion) in 35 projects in Ukraine. About 71 percent of the investment went

into private companies, 29 percent towards projects in the public sector. The EBRD is

committed to continue financing projects in Ukraine at

previous rate – about EUR 1 billion

per year.

Among other investors, multilateral international financial institutions (IFI) directly investing

in Ukraine are for example the IFC (the International Finance

Corporation , investment arm of

the World Bank), based in Washington DC and BTSB (Black Sea Trade and Development

Bank), regional EBRD-like institution, based in Thessaloniki,

Greece .

1.1.5. Demographics and labor force Bad news

! Declining population

The population of Ukraine is about 45 million (July 2012 est.), which is 6.3%

lower than

reported in 2001. To put the population number in prospective – Ukraine is seventh largest

country in Europe by population (after Russia, Germany, France, United Kingdom,

Italy and

Spain ).

Based on official statistics, the Ukrainian population has shrunk by 6.2 million people from

51.8 to 45 million since 1990. By contrast, the

Spanish population has grown by 8.5 million

from 38

.8 to 47.3 million people over the

same period. The

urban population is made up

69% of total population in 2010, with about 3 million people

living in Kyiv.

17

Bad news again

! Ukrainian population is not only declining, but also aging. 18

It is estimated that 77.8% of the population are Ukrainian and 17.3% are Russian. Minorities

include Belarusian, Moldovan, Crimean

Tatar , Bulgarian,

Hungarian , Romanian, Polish,

Jewish and others.

The

majority of the population is a member of one of the branches of the

Orthodox Church

(about 84%). Around 10% are

Catholic , while 4% are

Muslim , represented by Tatar who

mostly reside in the Crimea.

The labor force involved in the economy in 2011 was 22.09 million people with 15.8%; 18.5%

and 65.7% in the agriculture, industry and services sectors, respectively.

Official number

obviously does not include unofficially paid labor as well as Ukrainians working abroad and

sending their wages to support families back home.

Good news

! Among other advantages of investing in or doing business with Ukraine is its

workforce including:

High

scientific and educational potential -

powerful network of

universities and research

centers;

competitive qualified and skilled labor force.

For example, according to research company

Brain Bench, Ukraine ranks the 4th globally in

number of certified professionals in the

field of hi-

tech (being only behind United

States ,

India and Russia). (

http://www.brainbench.com/pdf/globalitiq.pdf )

1.1.6. New emerging industry Ukraine is known to

everybody as major producer of ferrous and nonferrous metals, also for

its coal mining, chemical industry, agriculture products including grain,

sugar beets,

sunflower seeds/ oil, vegetables, beef and

dairy products. It’s less known, though, as

emerging destination for Business Process Outsourcing industry (BPO).

In fact, Ukraine was ranked 32nd in Education on the

Legatum Prosperity Index of 104

countries – ahead of India, China,

Indonesia , Malaysia,

Mexico , Brazil,

Chile and other

popular outsourcing destinations. Ukraine has more than 800 universities and colleges

(

higher education institutions), over 1,000 IT companies and over 25,000

specialists involved

in IT outsourcing. According to Ukrainian Hi-Tech Initiative research, 16,000 IT specialists

graduate in Ukraine each year. Only 4,000-5,000 of them are

employed in companies that

provide professional IT services. The potential

remain huge, this number can easily be

doubled and Ukrainian government

takes strong initiative

aimed towards creating favorable

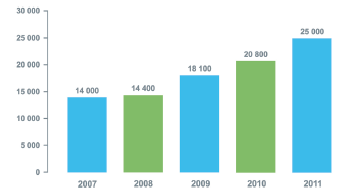

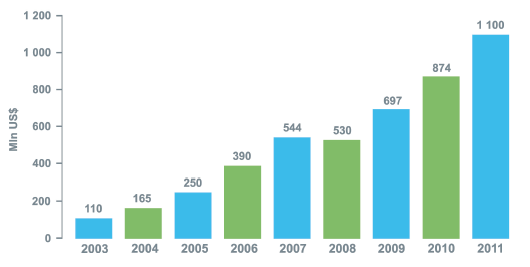

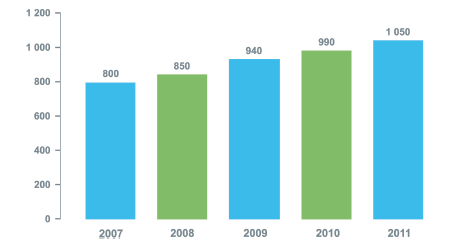

conditions for IT outsourcing business development. The chart below illustrates

development of Ukrainian IT industry measured by specialists employed in IT companies.

19

Source: Report Exploring Ukraine IT Outsourcing Industry 2012 Since year 2000 Ukraine has been one of the

leading players in software development

space and has been ranked at the top of IT outsourcing service providers in the global market.

According to BPM Watch, BPO sector (primarily in IT services) in Ukraine has grown

tremendously during the last 10 years (showing annual growth rate of 20-25%). By industry

experts estimations IT outsourcing sector reached USD 1.1 billion in 2011 (see

graph of the

volume of IT Outsorcing services 2003-2011) and

expected to

grow further in the next 5

years. Compared to other CEE countries strong in outsourcing (Poland, Romania etc as well

as Russia), Ukraine continuously reports the

highest rate of market growth.

Source: Report Exploring Ukraine IT Outsourcing Industry 2012 20

Ukraine entered the

offshore outsourcing market by providing software development

services in the early 1990s. Since then, the BPO market in the country has been showing a

steady growth as a result of demand from US and UK markets. While IT services remain to be

the main source of

revenue generation for the outsourcing industry in Ukraine, other BPO

projects like, FAO, HRO and KPO have also started to generate

considerable revenue for the

industry.

Some of the

reasons as to why outsourcing companies in Ukraine are reporting good

financial growth are discussed below:

Vast talent pool at low cost: The

literacy rate of Ukraine is 98% which is much higher

when compared to other offshore destinations. The country’s large pool of engineering

and IT talents has always been a key

factor in attracting foreign investors. Further, these

talents are available for the BPO companies at a lower cost. The salaries for the BPO

employees in Ukraine are

slightly lower when compared to other European BPO

destinations.

Cultural and physical proximity: Ukraine shares similar culture and business values with

that of US and other European countries. These prompt companies in US and Western

Europe to establish outsourcing

links with Ukraine BPO companies. The proximity in

physical

distance also

makes it a favorable near-shore destination for companies in US

and

Canada .

Political climate: Favorable political climate in the country is also a reason for the growth

of BPO sector. Recently the government as a measure to support outsourcing sector

cancelled the VAT for IT outsourcing companies and reduced their employees’ income

tax to 5%. The authorities are also very keen to

invest in infrastructure development

activities to

attract more foreign investments.

IP security : Ukraine is a country which has a high

respect for intellectual property

rights .

The country recently upgraded its IP

laws making them in par with the laws of other

developed nations.

(

http://www.bpmwatch.com/knowledgebase/know-emerging-bpo-destination-ukraine/ )

Language

skills remain the major limitation for Ukraine for BPO industry growth. In my

experience it’s very difficult to

hire a

person with right set of skills and good command in

English on top.

Seems that all foreign language speaking Ukrainians are already recruited by

call centers.

21

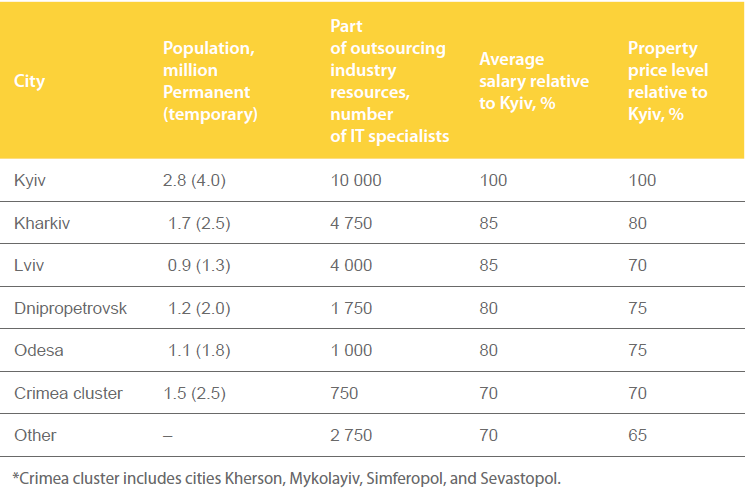

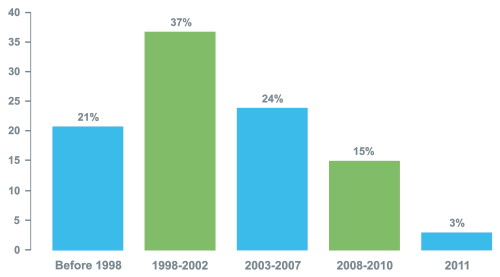

Regional Structure of Ukraine’s IT Outsourcing Industry

Source: Report Exploring Ukraine IT Outsourcing Industry 2012 Kiev

Kyiv region is the largest outsourcing and software development

center in Ukraine. A great

number of outsourcing companies operate

here , while 40 % of all ITO resources in Ukraine

are centered here. Kyiv boasts Ukraine’s largest IT talent pool. Currently, more than 10,000

highly qualified IT specialists are involved in the IT outsourcing sector. The city has 68

universities that prepare skilled IT personnel to provide outsourcing services.

Moreover , four

top-rated technical universities are

located in Kyiv (NTUU “Kyiv Polytechnic Institute”, Taras

Shevchenko National

University of Kyiv, National University of “Kyiv-Mohyla Academy”, and

National Aviation University).

Lvov

Apart from Kiev, I would only separately highlight Lviv, which is currently ranked as 3rd

outsourcing destination in Ukraine. Lviv, capital of western Ukraine is emerging as the

fastest growing outsourcing destination in Ukraine and one of the fastest growing in Europe.

The city of Lviv is a leading educational center in Ukraine and one of the largest in Central

and Eastern Europe with almost 40 higher education institutions, which

teach roughly

130,000 students. There are 26 top level universities, 5 of which prepare highly skilled

specialists in computer technologies. Over 1,000 IT graduates are supplied by

local 22

universities to the market annually. Currently, over 4,000 IT specialists are involved in the

Lviv’s IT outsourcing sector. According to the experts, this number is expected to grow by at

least 20 % annually, until 2015.

Comprehensive report on IT outsourcing industry in Ukraine is available for download at:

http://hi-tech.org.ua/wp-content/uploads/2012/08/Exploring-Ukraine-IT-Outsourcing -

Industry-20121.pdf

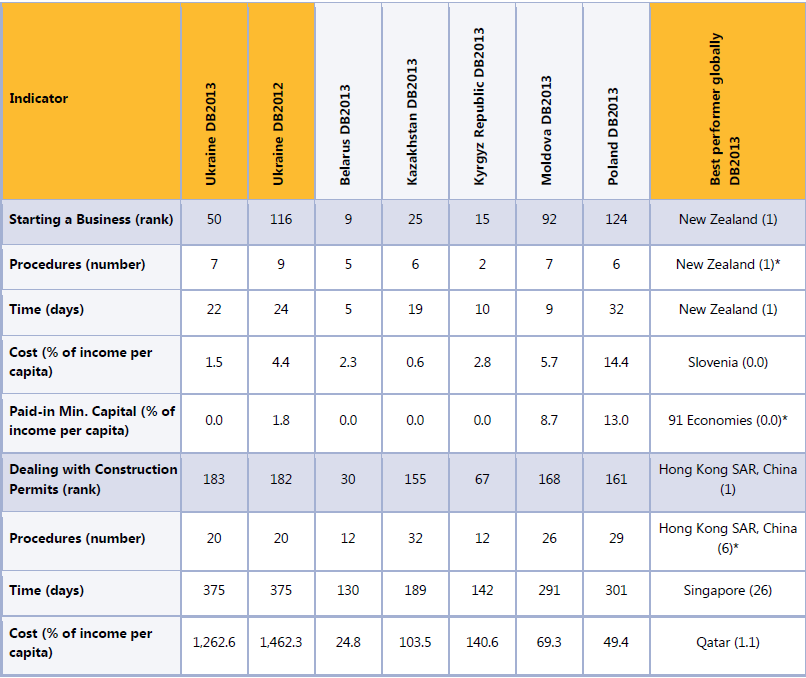

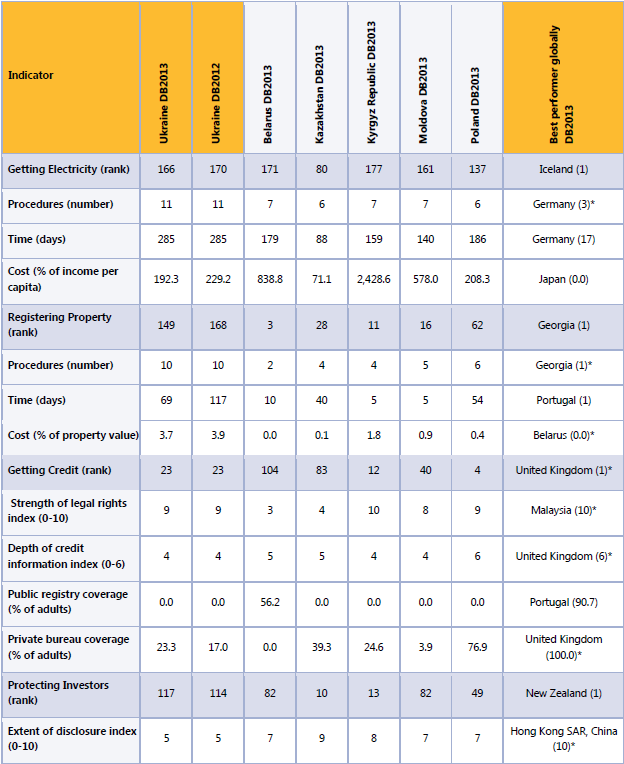

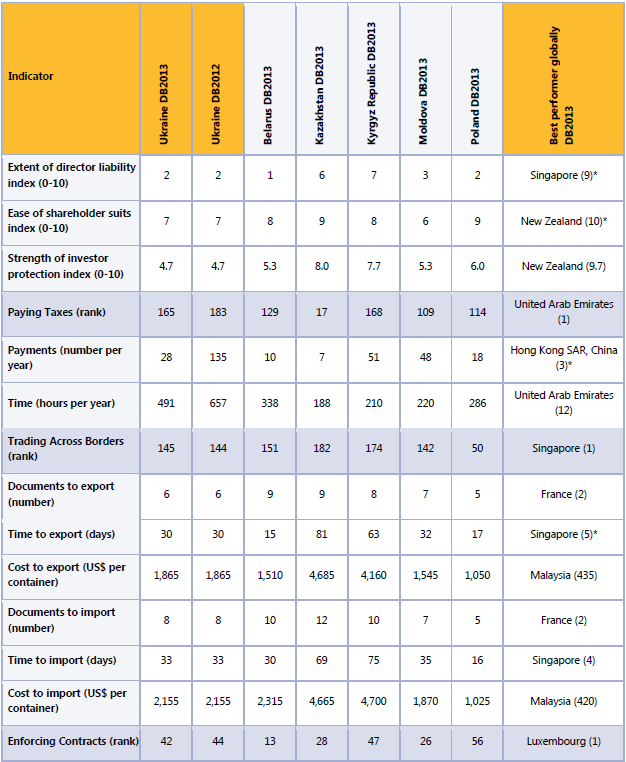

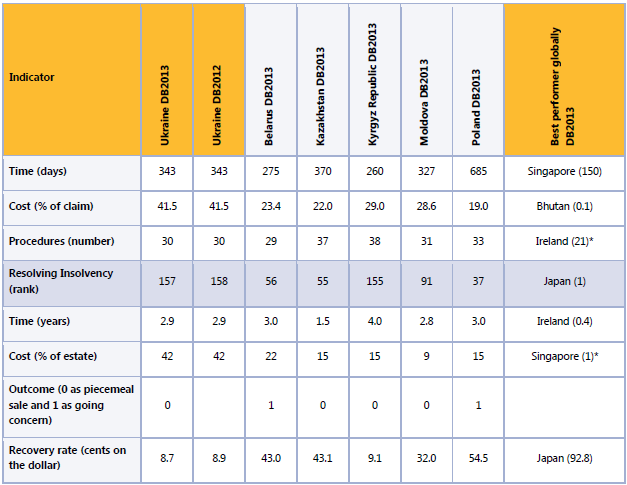

1.2. The Business Environment The World Bank and the IFC (International Finance Corporation) regularly analyze and

measure business environment in most of the countries. The

results of their research are

summarized in annual publications called Doing Business. It measures and tracks changes in

regulations affecting 11 areas in the life cycle of a business: starting a business, dealing with

construction permits, getting electricity, registering property, getting credit, protecting

investors, paying

taxes , trading

across borders, enforcing contracts, resolving insolvency and

employing

workers .

These publications

rank countries world-

wide (across 185 economies) by how easy of

difficult to

open and run a small to

medium -size business complying with

relevant legislation . Doing Business 2013 country specific reports, are available for download on the

Doing Business

website at

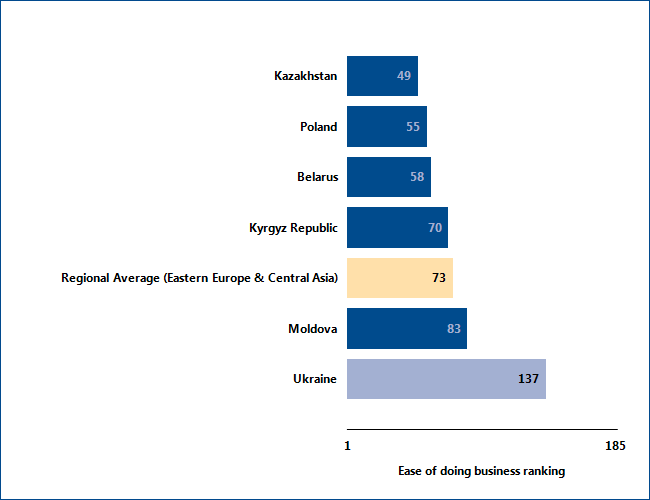

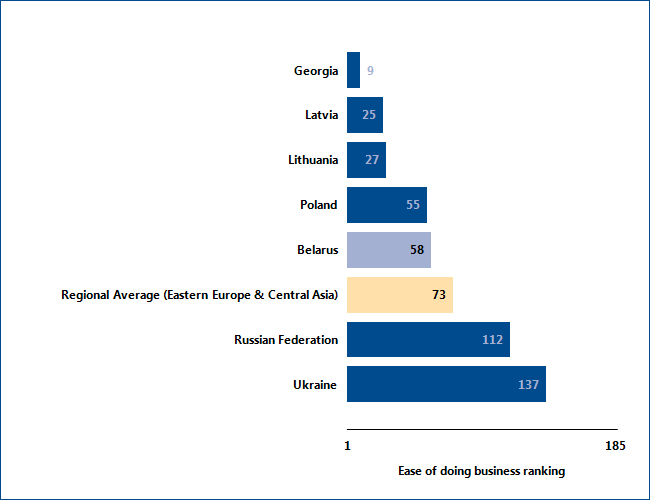

http://www.doingbusiness.org According to Doing Business 2013, Ukraine ranks 137 in the world on the

ease of doing

business benchmark.

Good news

! Ukraine’s rank improved 15 places

compare to 152 in 2012.

23

Source: Doing Business database.

The increase of Ukraine’s rank measured by Doing Business methodology is to great extent

related to gradual improvement of regulatory environment. Please review Appendix 2 for

Summary of Doing Business indicators for Ukraine. The summary compares Ukraine with the

closest peers and Best Performers globally.

In real life, however,

decisions to enter a new market or to start a business in a new country

are often made by businessmen taking into account other measures and factors, such as size

and proximity of the new market, expected demand, ease and cost of

logistics , price

arbitration , closeness of culture and

traditions etc. Quite often those reasons could also be

emotional like “jumping on bandwagon”, for example, fellow businessmen are running

successful operations in the

given market, a market growth or its size providing excessive

optimism, real estate

bubble etc.

Nevertheless, careful

study of the business and regulatory environment is by no

means less

important than a market research. Although, ranks and indicators of Doing Business

database and similar

studies might

seem like dry

figures , they do provide first information on

what to

expect when doing business in a country such as Ukraine or Belarus.

24

Having said that, I do not suggest, that a decision for a new market expansion, or investing

into foreign country should be based primarily on its rank of ease of doing business or

maturity of its business and regulatory environment. Very often business reasons

overweight in decision making. New markets may provide opportunities for foreign

businessmen via larger consumer base, market consolidation potential, low market

saturation or low-level consumption of a product, providing

therefore potential for growth

and so on. Yet, again, thorough

knowledge of the country’s business and regulatory

environment helps to

adjust expectations accordingly and start business prepared to what

otherwise might be costly surprise.

The above said is very true in

case of Ukraine and Belarus. These markets, Ukraine in

particular, attracted since its Independence and continues attracting a lot of

interest from

foreign investors. Complicated and often confusing business and regulatory environment,

official bureaucracy,

corruption and so on remains significant obstacles for foreign investors

and businessmen. Some have been successful and some decided to

pull out from Ukraine.

Corruption

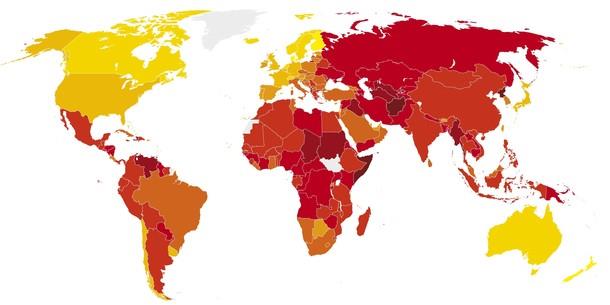

Corruption in Ukraine remains significant problem for businesses and the country’s image in

general. Ukraine was ranked 144th on the Corruption Perceptions Index 2012, compiled by

Transparency International, a global anticorruption non-government organization. Ukraine’s

rank slightly improved compared to 152 in 2011. For

comparison , Russia ranks 133d, Belarus

123d, Moldova 94th and Georgia 51st.

The index scores 176 countries and territories from 0 (highly corrupt) to 100 (very clean)

based on perceived levels of public sector corruption. Corruption Perceptions reports by

Transparency International are available at:

http://www.transparency.org/cpi2012/results 25

Source: http://www.transparency.org/cpi2012/results

Corruption in Ukraine significantly affects investment climate in the country as well as

foreign investors’ appetite towards investing in Ukraine. The EBRD, which is the largest

foreign investor in Ukraine, is

putting a lot of efforts and

pressure on Ukrainian government

and the

President trying to achieve commitment from government officials to fighting

corruption on all levels.

Please watch - EBRD President Suma Chakrabarti: Corruption in Ukraine must be fought on

all levels at

http://www.youtube.com/watch?v=MuFv1FtADUg 26

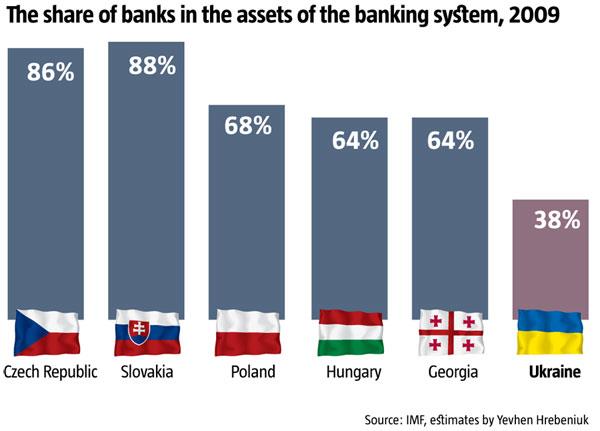

1.3. Banking system As of January 1st, 2013, Ukrainian banking system

consists of 175 banks. Despite significant

number of banks, the banking system is reasonably concentrated – assets of Ukraine’s 10

largest banks (measured by total assets) provided 53% of the banking system total assets as

of January 1st, 2013. Assets of Ukraine’s largest bank, Privatbank, were 15% of total assets in

the banking system as of January 1st, 2013.

Source: National Bank of Ukraine. http://www.bank.gov.ua

Foreign (European) interest in Ukrainian banks peaked during 2005-2008, with a

wave of

high-profile acquisitions on Ukrainian banks by European counterparts. Since 2009, more

and more European banks have left Ukraine, including ING Bank, Home Credit Group, Сredit

Europe Bank, Societe Generale, Volksbank International and

Swedbank . SEB Bank

sold assets to a Ukrainian businessman, and other banks simply left the retail market. The

outflow of foreign capital is having a

heavy impact on Ukraine’s banking system.

The 2006-2008 credit boom and the surge of loans issued in foreign currencies were fuelled

by cheap European money. However, the 2008-2009 crisis showed that the presence of

private Western banks in Ukraine was a vacation from bigger troubles rather than a burden

for the Ukrainian market. Capital inflow from Europe changed the

face of the Ukrainian

banking system for the better by improving bank service culture and

giving Ukrainians

broader access to loans than they had ever had. The tables turned when foreign banks

began to

lose ground to captive banks

owned by oligarchs that mostly lend money to their

own companies. This is a

sign of the growing strain on business in Ukraine.

The

massive inflow of European banking groups to Ukraine had a largely favorable impact on

the economy. Unlike the mining industry, where most FDI

comes from the oligarchs’

repatriated profits, European newcomers in the banking sector brought along new foreign

direct investment. According to the National Bank of Ukraine, only 7.7% of the cumulative

FDI into the share capital of Ukrainian companies went to the financial sector in 2004. In

2008, the figure was almost 30%. Over 2006-2008, nearly 42% of the $26 billion foreign

direct investment in Ukraine went to the financial sector as foreign interest in Ukrainian

banks peaked. European groups did not abandon their subsidiaries during the crisis. In 2009-

2010, they invested over UAH 17bn of new share capital in the Ukrainian banking sector,

which was 67% more than what the owners of local banks invested.

Another obvious

effect was the unprecedentedly broad access to retail lending available to

average Ukrainians from 2005-2008. The mortgage

loan portfolio alone swelled sevenfold

over 2007-2008, even though foreign banks preferred to place foreign exchange risks on the

27

borrowers. They issued the

greater share of mortgage loans in dollars. As a result, the

amount of bad loans soared in 2009-2010.

The inflow of European banks had a great

indirect positive impact on the banking sector and

Ukrainian economy

overall . First, they brought in new standards of corporate governance

and customer service. European banks in Ukraine have

clear rules for risk

management which, if violated, may result in the

firing of the local executives. Thus, a foreign bank will

never pick up deposits from the retail market to further

issue them as loans to

linked companies. By contrast, quite a few of their Ukrainian peers eagerly do this, revealing their

likely

status as captive banks of big business groups.

The owners of European banks are groups that have no companies in other industries. Their

interests lie in the

orbit of the banking business. It is

hard to imagine a situation where a

parent bank based in Europe instructs its Ukrainian subsidiary to issue a loan to a specific

company or to overlook the rules for issuing loans to one borrower or associated entities.

Unlike them, most bank owners in Ukraine have other

primary businesses and use their

banks as donors more than anything

else in times of crisis. Officially, they comply with the

NBU’s restriction on lending more than 25% of the regulatory capital to one borrower. Yet,

some sources suggest that the real level of

insider lending in some captive banks may exceed

50% of the total loan portfolio. The regulatory

authority does not

monitor the entities of big

business group owners deeply enough to determine this.

28

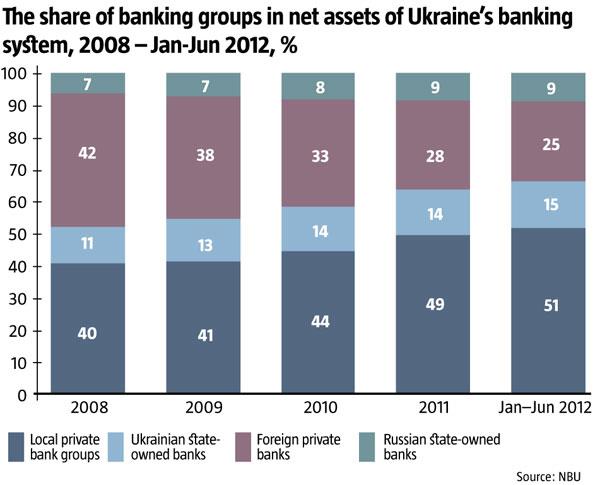

Source: www.ukrainianweek.com The

intense increase of the European share in the Ukrainian banking system over 2005-2008

has essentially squeezed captive banks to the sidelines. Some oligarchs even gradually

switched to using

universal European banks with high standards to service their companies.

It was definitely cheaper for them compared to maintaining and developing a bank of their

own.

Since 2010, Ukraine has seen a reversal of the European banking trend. The growing

pressure on businesses and resurgent fear of property loss have

once again fuelled the

demand for captive banks, just as they did in the 1990s and early 2000s. In a

prime example,

a

German group recently sold its Ukrainian bank to a local oligarch. On the whole, the share

of private Western banks save for state-owned Russian banks shrank from almost 42% in

early 2009 to 25% in the first half of 2012, mostly in

favor of local Ukrainian banks. A few

more banks with European capital may end up in the

hands of Ukrainian owners by the end

of 2012.

29

Source: www.ukrainianweek.com The expansion of Russian state-owned banks including VneshEconomBank (VEB), VTB and

others, has been a separate trend. State-owned banks operate in many countries and help

the government to

perform some

social functions . Obviously, Russian state-owned banks

have provided much broader access to loans for mostly big Ukrainian companies. This was a

positive

contribution to Ukraine’s economy. One of Russia’s most proactive banks is VEB

which is, in fact, a

quasi -bank regulated by a special federal act. Whenever a European

government becomes a

shareholder of a bank, it

sets some restrictions on the growth of its

assets, sometimes pressuring the bank to quit risky foreign markets. Quite the opposite for

Russian state-owned banks: they are actively expanding abroad thanks to financial resources

granted by the government at prices below market value. Essentially, this means that they

are building

networks in other countries at the expense of Russian taxpayers.

30

The financial sector is typically a

barometer for changes in long-term

investment expectations for Ukraine.

Even though foreign capital had been

present in Ukraine’s banking sector

before the 1998 crisis, 2005 proved to be

the real breakthrough year. Driven by

post-Orange Revolution exuberance,

European banks began to buy Ukrainian

banks one after another, often paying

sums that were several times higher

than what the actual assets of the banks

were worth at the time. In 2007, at least

10 Ukrainian banks found themselves in

the hands of foreign owners. Good deals

turned Ukrainian oligarchs into

dollar billionaires overnight – mostly because

of the overheated banking sector. The

prices paid for banks ranged from 2.6 to

almost 5 times their equity value – the

latter was paid for Praveks Bank. To

justify the gargantuan prices, the

purchased bank was expected to provide

sustainable

rapid growth in assets at

over 12% annually, a 20% annual ROE

increase and a 15% equity value growth.

The 2008-2009 crisis proved that these

had been unrealistic expectations.

Source: www.ukrainianweek.com Currently Ukrainian economy is on credit-based diet. Post-crisis, availability of debt in

Ukraine is very low. The credit diet resulted in inflation in Ukraine in 2011 slowing to 4.6%

from 9.1%, and consumer prices in January-November 2012 dropped by 0.4%.

On the other

hand , availability of credit is as much important for growth of economy as

blood flowing though human

body for life. In Ukraine, though, growth of total sum of loans

in economy was less than 3% in 2012. For comparison - the total growth of loans in 2006 was

31

71%, in 2007 it was 74.1%, in the crisis year 2008 it was 71.9%. Even in 2011 this indicator

looked much better, being 9.6% up.

In practice, small and medium-size enterprises in Ukraine have minimal access to bank

financing. As a consequence of the weakness of the steel industry and the near absence of

financing for small and medium-

sized enterprises, output contracted during the second half

of 2012. Even Prime Minister Mykola Azarov no longer expects growth in 2013.

As the result, the country has seen a triple deficit in 2012. As a result of a smaller economic

growth, the budget deficit in 2012 is expected at 2.6% of GDP, which is higher than the

target fixed at 1.7% of GDP. The current account deficit in January-November 2012 was

$12.443 billion, being 38% up year-over-year. The deficit of the balance of

payments over

the period grew by 41% year-over-year, to $3.336 billion.

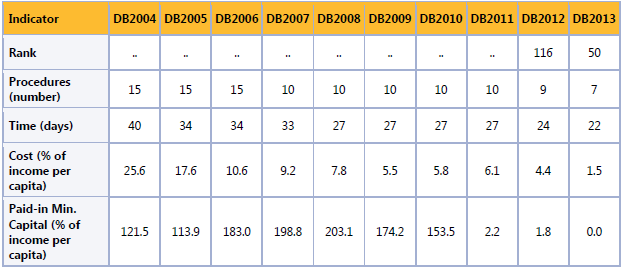

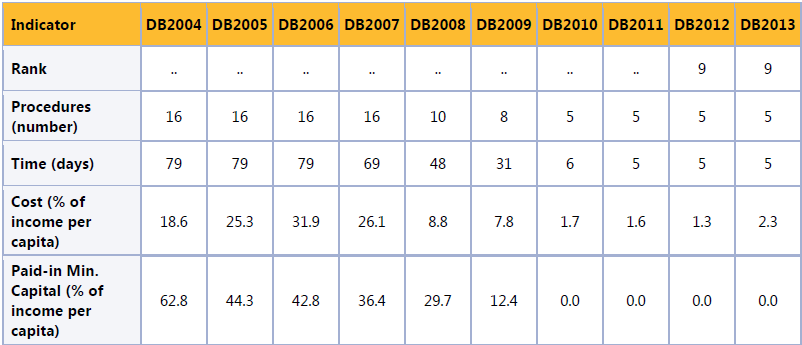

1.4. Starting a business in Ukraine Good news

! As the table below

shows , Ukraine developed a long way in improving

regulatory environment for starting a new business (

legal entity). Number of procedures,

time and cost of starting up the business decreased very substantially during last ~ 10 years.

Moreover, currently there is no minimum share capital requirement for LLC (most commonly

used form of business ownership).

Source: Doing Business database.

To

improve its competitiveness for investors, Ukraine has lately introduced a series of

legislative changes aimed at simplifying the start-up and conducting business. The changes

include the following:

establishment of a “one-stop shop” for corporate registration;

online access to the Unified State

Register (country-wide list of business entities and

individual entrepreneurs) and the Unified License Register;

32

abolishment of the

permit requirement for company seal production, and of the

requirement to notarize copies of

documents for registration

purposes ;

adoption of the model

charter , and

moderate simplification of the liquidation procedures.

Some of the declared changes are yet to be made operational (e.g., online corporate

registration). In

addition , mandatory licensing or other state authorizations were abolished

in many industry sectors; the “

silent consent”

concept and the declaratory principle (which

implies a company may undertake certain

types of business

upon making a relevant

declaration to the state authorities) were implemented instead of some licenses and

permits. In particular, procedures for obtaining a construction permit were simplified

significantly.

Source: KPMG. Your Business in Ukraine 2012

1.5. Market entry strategies Foreign investors can

consider the following options for entering the Ukrainian market:

direct sales;

agency and commission arrangements;

joint venture with a Ukrainian partner;

representative office and

Ukrainian subsidiary.

The choice made by the foreign investors is usually motivated by the incorporation and

maintenance costs (if any), as well as the legal and tax risks involved.

1.5.1. Direct Sales The simplest

option for entering the Ukrainian market (or majority of foreign markets for

that

matter ) is by way of direct sales contracts. A foreign legal entity which sells goods or

services to customers (or distributors) in Ukraine directly from abroad would not be

subject to Ukrainian taxes. Depending on the agreed terms of

delivery , the Ukrainian customers (or

distributors) would be responsible for customs clearance and would have to pay customs

duties and taxes (import VAT, excise) (if any).

A properly drafted

cross -border contract allows a foreign company to avoid taxation in

Ukraine. The possibility to

choose the foreign (likely domestic) law as the

governing law of

the contract makes direct sales a viable option for business. However, in choosing the

foreign law, the public

order rules and imperative norms of Ukrainian laws (e.g., currency

control regulations, etc.), must be complied with.

33

1.5.2. Agency and Commission arrangements Agency and commission contracts present another comfortable alternative for structuring

business in Ukraine. From a legal standpoint, such arrangements

allow a foreign company to

carry out commercial activities in Ukraine without

setting -up

permanent establishment in a

form of corporate

vehicle , employing personnel,

meeting accounting and reporting

requirements, as well as bearing all associated costs and risks.

Nevertheless, from a tax perspective, risk remains, that agency and commission contracts

may trigger taxation in Ukraine, specifically when an

agent acts exclusively on behalf of a

particular foreign company, and the supply of agency or commission services does not

constitute its

core business (e.g., as may be the case for securities,

insurance brokers).

Agency and commission contracts for activities of a preparatory or auxiliary

nature (such as

market research and

analysis ) should not generally create a permanent establishment of the

foreign entity, and

hence its profits would be taxed only in the country of tax

residence .

1.5.3. Joint venture with a Ukrainian partner Per the Ukrainian laws, a foreign investor is granted the right to enter into a joint venture

with a Ukrainian partner (formally referred to as “a joint

activity agreement”, which can take

the form of a simple partnership agreement, a joint production, or a joint co-

operation agreement with a Ukrainian partner(s)). Investment of this kind is subject to state

guarantees and should be registered with local state authorities of Ukraine.

1.5.4. Representative office (commercial and non-commercial) Day-to-day business in Ukraine can also be carried on through a representative office (“RO”).

A RO is not a legal entity but a

division of a foreign company registered in Ukraine. Its head

office assumes all rights and obligations of the RO and bears the liability for its

actions .

A RO which carries out commercial activities in Ukraine is deemed to be a commercial RO

(which in

different jurisdictions is called a “

branch ”) and triggers a permanent establishment

of the foreign company for tax purposes. This, in turn, implies that, if a relevant

double tax

treaty is in place between Ukraine and the foreign company’s tax residence jurisdiction, only

a portion of the company’s profits, which are attributable to the RO, will be taxed in Ukraine.

A RO which undertakes activities of a preparatory or auxiliary nature usually does not create

a permanent establishment and is not subject to corporate income taxes in Ukraine.

Generally, a RO would be subject to registration in the Ministry of Economic Development

and Trade, the State Tax Service, the State Statistics Services, and the State Pension Fund. A

34

foreign bank’s RO

shall be registered with the National Bank of Ukraine. However, the list of

registering authorities may be

expanded due to specific industry particularities. The

registration period takes up to 3 months following

submission of all necessary documents.

The

preparation of documents may take additional time as in many

cases they would

require approval , notarization, and/or legalization.

1.5.5. Ukrainian subsidiary A foreign company may choose to establish a Ukrainian subsidiary for doing business in

Ukraine. A Ukrainian subsidiary controlled by foreign companies or nationals, generally

enjoys the same legal treatment as legal entities without foreign participation. Such

company, with minor limitations justified by national interests, may enter into agreements,

assume legal obligations, acquire property, as well as sue and be sued in its own name. It

may

engage in any commercial activity envisaged in its charter (

articles of incorporation).

It’s important to

note that non-

resident entity (foreign) or 100% owned Ukrainian subsidiary

of non-resident

cannot own land in Ukraine. A non-resident or 100% owned Ukrainian

subsidiary of non-resident, can on the other hand, own land if the land is

part of a property –

real estate

object , which has a registration in Real Estate Register. From my personal

experience, I can suggest that in case a non-resident company or 100% owned Ukrainian

subsidiary of non-resident company must acquire a land in Ukraine, the limitation can be

solved by

selling 0.01% ownership to a resident company or physical person – usually a

trustable

manager or

lawyer . We have been advised by local legal counsel this structure (and

it indeed worked out) when local 100% subsidiary of the

client of mine was acquiring a land

plot for a Greenfield

factory construction

project . Following completion the project, the

factory was registered in real estate register (including the land plot) and the above

mentioned structure was not

anymore required .

1.6. Foreign investment treatment Most business areas available on the Ukrainian market are open to foreign investors.

However, foreign investors’ access to certain economy sectors is forbidden or restricted,

namely:

in the media industry, foreign investors are not

allowed to be founders of

television and

radio companies or sole founders of information agencies; the share of foreign

investments in a Ukrainian information agency may not exceed 35 per

cent ; foreign

investors may not

hold more than 30 per cent of shares in a Ukrainian publishing house;

foreign investments are prohibited in the armament, explosive,

launch vehicles

development, production and

handling industry, as well as in other areas of national

interest;

foreign investors may not own agricultural land in Ukraine (even if they inherit it).

35

In addition, foreign investors who wish to acquire/increase a significant

shareholding in a

Ukrainian bank are required to submit some additional documents before approval by the

National Bank of Ukraine may be granted.

The Law of Ukraine “On Foreign Investment Treatment” defines “foreign investment” as an

investment made by a foreign investor (foreign individual or company) in compliance with

the Ukrainian laws for

profit generating purposes or for achieving a social effect. Under the

Ukrainian investment laws, foreign investments may be made in a variety of forms,

including:

establishment of a company (“Greenfield investment”) by the foreign investor

solely or

jointly with a Ukrainian partner;

acquisition of stock (shares) in an existing Ukrainian company (a Ukrainian company with

foreign investments constituting at least 10% of its share capital is deemed to be a

“company with foreign investments”);

acquisition of other types of securities (except for promissory

notes );

acquisition of movable or immovable property in Ukraine;

acquisition of the right to use land and/or to

exploit natural resources;

joint venture with a Ukrainian partner (not associated with incorporation).

Generally, registration of investments is not required, but might be advisable in certain

instances. For instance, if a foreign investment is made in kind (i.e. as a contribution of fixed

assets into share capital) the contributed fixed assets may be exempt from import customs

duties provided the relevant investment is registered with the Ukrainian authorities.

In practice, though, in-kind contribution of fixed assets (typically machinery & equipment ) to

be exempt from import duties requires a lot of work with customs officials and submitting a

lot of various documents. It can be especially challenging if equipment is being imported in

Ukraine in several deliveries. In my experience, we have managed to organize delivery of the

equipment efficiently to avoid keeping the trucks at the customs for long time. The trick for

us was to get one unified custom code for the entire equipment for the factory. In such case

in-kind contribution will be exempt of customs duties. Custom duties on various products vary

between 4 and 8%, so doing extra work with customs may be worth it, depending on size of

the investment.

However, if the assets invested are

disposed of within three years following the

date they

have been recorded in the

books of the Ukrainian entity, all

applicable import duties should

be paid to the Ukrainian budget.

36

In general, the Ukrainian investment

protection legislation stipulates national treatment for

all investors and investments in Ukraine (with some

exceptions imposed by specific laws).

Domestic legal safeguards available to foreign investors include:

“grandfather

clause ” against

adverse changes in the basic legal treatment of investments

(as set out in the law of Ukraine “On Foreign Investment Treatment”);

prohibition of nationalization;

prohibition of expropriation not justified by evacuation / rescue measures taken in

connection with disasters, accidents or epidemics, as well as judicial redress against a

decision to expropriate the investment;

expedient, adequate, and effective compensation for damages (including

lost profits and

non-pecuniary damages)

incurred as a result of actions or omissions of the state

authorities and their officials, as well as compensation for the value of the expropriated

investment;

time limitation (6 months) for

return of the investment (including profits gained), etc.

In practice, though, it might be difficult to

challenge actions or omission committed by the

state before national courts.

Ukraine maintains more than 50 bilateral investment treaties (“

BITs ”) concluded with

countries from the

Americas , Europe, Asia, etc (including with Estonia since 1995). In line

with modern international practice, BITs sustain an effective

tool in the hands of foreign

investors to defend themselves against arbitrary and discriminatory measures of the state

authorities. Most of Ukraine’s BITs

contain clauses granting a “most favored nation”

treatment and national treatment to foreign investments and investors.

Importantly, Ukraine has acceded to the 1965 Washington

Convention on the Settlement of

Investment Disputes between States and Nationals of Other States, which provides an

opportunity for foreign investors to challenge actions of the state before the International

Center for Settlement of Investment Disputes (“ICSID”). For certain advantages of the ICSID

proceedings, see

Section “Dispute Resolution” below.

1.7. Corporate forms Common corporate structures – pros and cons

In Ukraine, common corporate forms are a limited liability company (“LLC”) and a joint stock

company (“JSC”), which are to some extent are comparable to Estonian forms OÜ and AS.

Ukrainian laws provide for certain other corporate structures, which are rarely used due to

their undetermined legal status or practical inefficiency.

Registration 37

Unlike an LLC, a JSC is entitled to issue shares which are subject to registration with the

National Securities and Exchange Commission (“Securities Commission”). Due to this

peculiarity, the timing for registering an LLC is shorter (3-4 weeks) than for a JSC (2-4

months).

In the majority of cases, foreign businessmen

prefer to set up an LLC rather than a JSC, in

Ukraine. Similarly to a JSC, the liability of LLC’s shareholders (participants) is limited to their

investment in the share capital. In addition, requirements as to the incorporation and

operation of an LLC are simpler and more straightforward than those of a JSC. A Ukrainian

company (either LLC or JSC) should be registered with the state registrar, tax, social security

and statistical authorities.

Number of shareholders

An LLC may be established by a sole shareholder unless the latter itself is

held by a sole

shareholder. A person is not allowed to be a sole shareholder (

participant ) of more than one

LLC.

Interestingly enough Ukrainian legal system allows avoiding these limitations by splitting

ownership to 99.99% and 0.01%,

as learn from personal experience.

When the number of LLC shareholders exceeds 100, it shall be transformed into a JSC. A JSC

may be either public (when its shares are traded publicly) or private (when its shares are

privately held).

Minimum share capital

Currently, there is no minimum share capital requirement for an LLC. Founders of an LLC

should contribute 100% of the declared share capital in