TRADERUN

MOODUL TRADERUN

MODULE BUSINESS PECULIARITIES IN THE EU,

RUSSIA AND

EASTERN PARTNERSHIP COUNTRIES

ÄRI ERIPÄRAD EUROOPA LIIDUS, VENEMAAL JA IDAPARTNERLUSRIIKIDES

Lecturers: Ryhor Nizhnikau (

responsible ) Giorgi Gaganidze,

Sergei Proskura, Andres Assor

P2EC.00.202 (UT

code ), RIE 7044 (TLU code)

Reading materials: Business peculiarities in Russia

Lugemismatejal: Äri eripärad Venemaal

Created by Sergei Proskura Tartu 2013

TABLE OF CONTENTS

INTRODUCTION ....................................................................................................................................... 3

1. LEGALIZATION OF A COMPANY WITH A

FOREIGN OWNER IN RUSSIA ....................................... 4

1.1.

Laws ............................................................................................................................................. 4

1.2.

Documents for

registration of the company ........................................................................... 5

1.3.

The Head of the new company ............................................................................................... 6

1.4.

Payment of the authorized capital of the company ............................................................... 6

1.5.

Address of the company ......................................................................................................... 7

1.6.

Activities of the company ........................................................................................................ 7

1.7.

Seal .......................................................................................................................................... 8

1.8.

Branch office accreditation ..................................................................................................... 8

2.

FORMS OF INCORPORATIONS (

TYPES , PROS AND

CONS ) ......................................................... 10

2.1.

Private

Entrepreneur ............................................................................................................. 11

2.2.

Limited

Liability Company ..................................................................................................... 11

2.3.

Closed

Joint -

Stock Company ................................................................................................. 13

2.4.

Company name ..................................................................................................................... 14

2.5.

Comparison of

different forms of incorporation of

companies ............................................ 15

3.

TAXATION , DUTIES AND EXCISES .............................................................................................. 17

3.1.

The

essence of the tax system, the principles and

functions of

taxes .................................. 17

3.2.

The main taxes ...................................................................................................................... 20

3.3.

Tax rates in 2013 in Russia .................................................................................................... 22

4.

LABOUR RELATIONS (

INCLUDING IMMIGRATION LAWS) ......................................................... 25

4.1.

Entry and

stay of foreign citizens in the

Russian Federation ................................................ 25

4.2.

Types of visas for foreign citizens in the Russian Federation................................................ 25

4.3.

Migration Registration of Foreign Citizens in the Russian Federation .................................. 28

4.3.1.

The procedure for bringing the

work of

highly skilled professionals (VKS) ...................... 30

4.3.2.

Your work permits for foreign citizens arriving in Russia in the

visa -free

regime ............ 33

4.4.

Responsibility for violation of immigration laws ................................................................... 34

5. BANKRUPTCY/

CLOSING DOWN THE COMPANY ....................................................................... 39

5.1. The procedures applied in the bankruptcy ................................................................................ 39

5.2. Fictitious or deliberate bankruptcy ............................................................................................ 42

5.3.

Criminal code......................................................................................................................... 42

6. ALLOWANCES/ PERMISSIONS NEEDED, PROCEDURES TO ACQUIRE ........................................ 43

6.1. The privileges granted to foreign investors ............................................................................... 43

6.2. Excise duties ............................................................................................................................... 45

7.

ACCOUNTING ............................................................................................................................ 49

7.1 Levels of the system of accounting

regulation in the Russian Federation ................................ 49

7.2. The Federal Law "On Accounting" ............................................................................................ 51

7.3.

Chart of

accounts and

other documents .............................................................................. 52

7.4.

Russian tax system ................................................................................................................ 53

7.5.

Banking system in Russia....................................................................................................... 53

ABOUT TRADERUN

PROGRAMME ......................................................................................................... 55

2

INTRODUCTION The

current reading

material focuses on the business peculiarities in Russia.

***

The aim of the Traderun programme course “FUNDING PROJECTS IN RUSSIA AND EASTERN

PARTNERSHIP COUNTRIES” is to provide the students with comprehensive and practical

overview of the fundraising possibilities in EU and Estonia. The course gives an overview of

EU structural support and regional implementing agencies, that are available for a

businessman to apply for a fund.

A successful student will be aware of and understand the EU fundraising possibilities in the

frames of cooperation with Russian and Eastern Partnership countries, and able to define the

financing criteria and priorities.

The current reading material summarises the main aspects covered by lectures and

structurises the information channels for the future.

The course supports the other Traderun courses, especially the course related to EU

cooperation with Russia and Eastern Partnership Countries.

3

1. LEGALIZATION OF A COMPANY WITH A FOREIGN OWNER IN RUSSIA Today the investment attractiveness of Russia is very high. In

addition to the

dynamic pace

of

development of the

economy , Russia

offers to foreign investors increasing every

year the

market of

goods and

services to consumer and business. Most often, this together with the

high

rate of

return on invested capital is a crucial

factor in the

decision to enter the Russian

market.

One possible way to

full implementation of business activities on the territory of the Russian

Federation - is the

creation of a

legal entity.

An enterprise with foreign capital - is created on the territory of the Russian business-

organization whose founders are foreign citizens or

organizations . Russian

legislation provides for the

establishment of

enterprises in Russia as a 100-

percent foreign ownership

and joint - with the participation of Russian and foreign shareholders.

Established on the territory of the Russian Federation entity with absolute or partial foreign

ownership will operate

within the

framework of the Russian legislation. That is, the laws of a

foreign

investor is limited to a

choice of the legal form of the enterprise, defined deadlines

for accounting and tax reporting

rules for transactions and other mechanisms for

making and

processing of business transactions.

Forms of organization of business organizations:

Public joint-stock company (otkrytoe akcionernoe obshchestvo, OAO).

Private joint-stock company (zakrytoe akcionernoe obshchestvo, ZAO).

Limited liability company (obshchestvo s ogranichennoj otvetstvennost'ju, OOO).

Association and

others .

1.1. Laws The main laws

governing the establishment and

operation of organizations in Russia (as with

foreign capital, as

without foreign capital)^

Civil Code, from 30.11.1994 № 51-FZ (the last version of 11.02.2013)

Companies Act, of 26.12.1995 № 208-FZ (the last version of 05.04.2013)

The Law on Limited Liability Companies, from 08.02.1998 № 14-FZ (the last version

from 29.12.2012)

On state registration of legal entities and

individual entrepreneurs, from

08.08.2001 № 129-FZ (as last amended on 29.12.2012)

4

1.2. Documents for registration of the company In

order to

register a company with foreign capital in Russia, it is

necessary to

carry out the

whole range of legal

actions that you want to implement Russian citizens in the registration

of legal entities without foreign participation. In addition,

there are some nuances

associated with the

special status of foreign shareholders.

To register a company with foreign capital must provide an expanded list of documents

compared with a

package of documents necessary for the registration of organizations with

Russian capital.

Consider the example of a package of documents on registration of a limited

liability company (LLC).

If the founder are individuals:

Document confirming payment of state

duty for registration of a limited liability

company, 4000 rubles (≈ EUR 100);

Decision on the establishment of the founders LLC (Minutes of the founders);

Application for state registration of the LLC in the form approved by the

Government of the Russian Federation (includes registered office of creating

company);

Charter Company (

Memorandum and

Articles of Association);

List of participants of the company, if the participants more

than one;

Notarized

translation of the passport (

identity card) in Russian, made in Russia (not

in a foreign

country );

If the

residence of a foreign

citizen in a foreign country is not listed in the passport,

certified translation of the document confirming the address of permanent

residence, the Russian

language , made in Russia (not in a foreign country).

If the founder are the legal entities:

Document confirming payment of state duty for registration of a limited liability

company, 4000 rubles (≈ EUR 100);

Decision on the establishment of the founders LLC (Minutes of the founders);

Application for state registration of the LLC in the form approved by the

Government of the Russian Federation (includes registered office created Ltd.);

Charter Company (Memorandum and Articles of Association);

List of participants of the company, if the participants more than one;

Copy of the document confirming the state registration (

Certificate of

Incorporation or

equivalent );

An extract from the commercial register (or its equivalent), which contains

information about the foreign legal entity;

5

Notarized translation into Russian of the listed documents, made in Russia (not in a

foreign country);

Certificate from the

bank about the

account to confirm the investor's

ability to pay;

Certificate on tax number in the country of non-

resident ;

Power of

attorney for the

person responsible for signing the necessary documents

for opening accounts and registration of the LLC with foreign investments.

The

above documents is not

complete ,

since the registration of companies with 100%

foreign ownership and equity participation, there are some differences (other than the

contents of the package of documents depends on the list of founders of the legal entity).

We should also

focus on

such features of the Russian legislation:

1.3. The Head of the new company In Russia adopted the

basic name of the head - "General

Director " (CEO) (mostly used) and

the "Director". Appointment of Head of the newly created company - at the time of

registration of the legal entity they must necessarily be a citizen of Russia. If the founders

originally planned this way, and with the continued activities of the company will not have

any problems. But if it is assumed that the

firm created should be headed

alien , after its

state registration must be registered at the

Employment Center and get the

permission of

the Federal Migration

Service on the

admission of foreign

workers (

both the company and its

future foreign director).

Appointment to the post of Director-foreigner immediately

upon creation of the company,

without obtaining permission mentioned, is a gross violation of immigration laws. Permitting

Federal Migration Service is a very complicated procedure, which will be discussed in Lecture

4.

1.4. Payment of the authorized capital of the company For different

organizational forms of companies have different

terms of payment of the

authorized capital. For a limited liability company 50% of the

share capital must be

paid up

to the

date of state registration of the company. The remaining

part must be paid within 1

year from the date of incorporation. For the company (Public joint-stock company or Private

joint-stock company) 50% of the share capital must be paid no

later than 3 months from the

date of state registration of the company. The remaining part must be paid within 1 year

from the date of incorporation. Payment of the authorized capital can be made both in

cash and

assets of the founders.

6

Payment of the authorized capital up to the moment of state registration of the company

made the

following ways :

money - by opening a temporary bank account from which you made after the

registration of the founders of the money is transferred to the main account of the

company;

estate - by transferring the property to the Head of the company (CEO) under the

act temporarily, and after checking company founders made by the head of the

property is transferred by an act of the company.

1.5. Address of the company The law does not

require documentary

evidence of the

location of the enterprise (exact

address) in the territory of Russia in his account, but later on, in the course of business, the

company will need to have the document on the

basis of which its registration is made at a

specific address specified in the statute.

Such a document can be:

certificate of ownership of any non-

residential premises

lease office (

production ) of non-residential premises (

usually with a copy of the

certificate of ownership of the lessor's premises);

Registration is also possible at the address of permanent residence (residence registration)

on the territory of St. Petersburg and the

Leningrad region of its head (CEO).

The tax authorities have the right to inspect the actual location of the company at the

address specified in the statute. In the absence of registration at the company

could be

fined in the

amount of 5,000 rubles (≈ EUR 120).

Most often, the

fact of being the company's registered address is checked by

banks , customs

authorities and leasing companies.

However , a recent

increase in the address verification by

the

security services of

major Russian companies with state participation. For major tenders

for the

supply of goods or services for the implementation of large companies such checks

can be carried out in

secret .

1.6. Activities of the company Any commercial organization in Russia may

engage in any

activity that is not prohibited by

law. Of the individual activities

required to obtain licenses (for example, passenger

transport, trade in

alcohol ,

mining , educational activities). Main activities of the company

are declared at check-in and

specify the unified state register of legal entities. Moreover,

there is the

concept of "core business". The main

purpose - to determine the amount of the

premium social security of workers.

7

In the future, you can

change as many

times as the main activity. The procedure for

changing it

takes a

period of 7

days and require the payment of the state fee of 800 rubles (≈ EUR 80).

Each activity is indicated by the statistical software. Full list of

states in the classifier NACE

(National Classification of

Economic Activities) (in Russian transcription is “OKVED”).

It is always desirable to specify the exact name of the activity in

accordance with the

qualifier that there was no refusal to register the company on

formal grounds .

1.7. Seal Every commercial organization in Russia is

bound to have a

round seal. Seal is not registered

anywhere,

manufacture seals deal with a lot of companies - enough to

express your wishes,

and you manufacture any seals. A reprint of a round seal is required at the bank and the

customs authorities. The company also has the right to have an unlimited amount of any

stamps and use

them on your own. However, all the basic documents of the company must

be certified by a round seal it. For example, the notary does not notarized document without

the round seal.

1.8. Branch office accreditation It is necessary to distinguish the creation of companies with foreign investments from the

opening of a branch office accreditation of a foreign legal entity in Russia. This branch - is a

separate subdivision of a foreign legal entity located

outside of its location and performing

all or part of the functions, including the

function of representation. Registration is

done by a

branch of its accreditation in the

manner determined by the Government of the Russian

Federation. The branch is

considered to be accredited if the information on it is listed in the

state register of branches of foreign legal entities.

Stages of registration of the company with foreign capital:

1. Founders are

holding a

meeting of the founders,

develop bylaws, sign the

necessary documents (minutes of the meeting and the Articles of Association).

2. The head of the notary signs the application for registration of the company.

3. The founders (one or all at

once )

issues the power of attorney to the representative

of conducting to supply and

delivery of documents to the tax office.

4. Founders paid registered capital in cash or property.

5. Any person (the head of the company (CEO), the founder of the company or a

representative by the power of attorney) pay the state fee for registration of the

company.

6. The representative of the founders of the company passes to the tax office all

documents for the registration of the company.

8

7. Federal Tax Service carries out the state registration of the legal entity. Carried out

simultaneously with the registration of tax registration, obtaining codes of State

Statistics

Committee , registration with the

Pension Fund, the Social

Insurance Fund

and the Fund of obligatory

medical insurance.

8. The representative of the founders of the company receives the documents after

registration.

9. The head of the company (CEO) or a representative of the

proxy opens a bank

account.

After committing all of

these activities, the company is a registered business entity, and may

work legally.

Some of the timelines:

Registration with the Tax Authorities 5-7

working days

Company Seal production 2 working days

Registration with the State Statistics Committee, with the non-budgetary funds

(Pension Fund, Social Insurance Fund, Obligatory Medical Insurance Fund) is done

by the tax authorities

Opening of bank accounts depends on the bank

Registration with the Federal Service for Financial Markets of

shares emission 30

working days

Limitations of foreign participation

There are features and limitations of participation of foreign investors in Russian companies.

Such features are set for the banking and insurance activities in these areas, the state

provides certain restrictions for foreign investors. There is also a restriction on the

purchase of shares by foreign investors, the largest Russian companies with state capital (

Gazprom ,

Rosneft and others).

9

2. FORMS OF INCORPORATIONS (TYPES, PROS AND CONS) Starting your own business, it is

important to

choose the

best form of incorporation of the

enterprise. Currently in Russia there are different forms of business enterprises as well as

private enterprise. This lecture will address the most common form of the creation of the

business, as well as a

brief description of all existing forms of incorporation of companies in

Russia.

Key used form of business organization in Russia:

Individual Entrepreneur (individual’niy predprinimatel, IP);

Limited Liability Company (LLC) (obshchestvo s ogranichennoj otvetstvennost'ju,

OOO);

Closed Joint Stock Company (CJSC) (zakrytoe akcionernoe obshchestvo, ZAO).

Each of these forms has advantages and

disadvantages .

Selection of a

particular form of

incorporation of the enterprise depends on many different factors. The set and the

effect of

these factors are different for different types of businesses.

For example,

before the start of the business may have some

questions :

Do you like independence?

Do you want to start a business with

someone else ?

Are you willing to provide a large document in the company?

Are you

going to buy large quantities of goods on

credit ?

Are you able to independently make the required amount of capital?

As is often the

case , you may

find that your answers suggest

several possible solutions. You

will also, eventually, will have to choose the best form of incorporation of your company.

The answers to the above questions may

lead to the following conclusions:

You have decided to conduct a joint business activities. Do you want to start a

business with someone else, then you should think about the Closed Joint Stock

Company or a Limited Liability Company.

Your

sales activity is associated with a

greater risk, it may be

wise to think about

the Closed Joint Stock Company.

If you

cause difficulty maintaining the register of shareholders and additional

reporting on the shares, you should choose a Limited Liability Company.

You are going to buy large quantities of goods on credit, then it is better to

choose a Closed Joint Stock Company.

Some of the findings may

seem contradictory. All the

same , the

final selection of the optimal

variant is

yours . It is necessary to analyze the pros and cons.

10

First , try to understand what

lies behind the

term "Private Entrepreneur":

2.1. Private Entrepreneur Private Entrepreneur - is a natural person who is engaged in business activities

independently.

NB! Private Entrepreneur can only be a citizen of Russia, so in the context of this lecture,

this form of business is irrelevant. However, some consider this form.

Private enterprise has its advantages:

a minimum of organizational formalities;

a minimum of accounting documents;

economic independence;

there is no need to make share capital (at registration is not required).

The main disadvantage of an Private Entrepreneur is that it is liable for its obligations with all

its assets.

Serious problems can

arise from a private owner in the event of his

illness or

absence from. If not pre-think the

issue may be in trouble.

Now let us consider

another legal form of the enterprise - the limited liability company:

2.2. Limited Liability Company Many companies use this particular form of incorporation. Limited Liability Company is a

grouping of

physical and (or) legal entities for joint economic activities. The authorized

capital is

formed only

through the contributions of the founders. The minimum capital of

10,000 rubles (≈ EUR 250). Limited Liability Company is a legal entity and has its own name.

All

members of a Limited Liability Company is liable for its obligations within their deposits.

This distinguishes this form of incorporation of a Private Entrepreneur as an Private

Entrepreneur

shall be liable for its obligations with all its assets.

The main

advantage of a Limited Liability Company is that the solvency of each

participant in

the company's obligations is limited to the amount contributed by them to the authorized

capital in accordance with the contract. This is significant in that case, if you're going to take

large amounts of money on credit or a large number of goods to market, or is

planning to

implementation any risky business transactions. Limited Liability Company continues to

exist even if some of the participants decided to withdraw from it or died. This does not

affect the

state of society as a whole. Another advantage is that your

children can participate in a

given society is inherited.

But this form has some shortcomings:

any deal for the transition of ownership of the share capital (

sale , donation, etc.)

must be notarized;

11

significantly

increases the time for the issue of a large number of accounting

documents;

every time you have to disclose the

details of their business, presenting to the

authorities the necessary financial documentation

all founders of agreement to make a

total of

half of the share capital at the time

of registration.

How to register a Limited Liability Company?

This can be done in three ways:

1. You can register a Limited Liability Company on their own,

2. You can contact the law firm which is engaged in business registration, and

setting out their demands, they can issue a Limited Liability Company,

3. You can buy

ready -made Limited Liability Company.

Self-registering your

costs will

include :

state fee for registration of a company in the tax office (4000 rubles) (≈ EUR 120);

payment notarized signature on the application for registration of the company

(≈ 1,000 rubles) (≈ EUR 25);

payment of at least 50% of the share capital (min≈ 5,000 rubles) (≈ EUR 125);.

If you go to a law firm, your costs will be about three times as much, but the time for the

preparing registration of the enterprise significantly reduced.

If you buy a ready-made company, the

cost will be about the same, registration will take a

bit of time, in which case you get someone else's articles of association, someone else's

name, etc., and if you later want to change

something , it will require additional costs.

According to statistics, the

majority of Russian entrepreneurs prefer to conduct business

registration through specialized law

firms . It is most likely due to the

complexity of filling

special forms for registration of the company. Before you expand business operations and

begin to fill in the

relevant financial documents, consult an

accountant who can give you

good advice about the establishment of the accounting profession in your enterprise. This is

no small

matter , as the director is responsible for the state of accounting at the enterprise.

The Limited Liability Company has been

operating under a Statute.

The Statute includes:

the name and type of society;

the

object and purpose of economic activity;

size of the authorized capital;

provision of limited liability;

management structure and governance;

order of reorganization and liquidation, etc.

The Statute must

contain all the main features of:

type of society;

12

the object and purpose of its activities;

the founders;

name and location;

size of the authorized capital;

economic activities;

procedures for

calling and conducting meetings;

rights and duties of the director;

change the order of the director and his term of office;

rights and obligations of the company;

describes how the financial

control and the

dividend is declared, the procedure

for their payment;

description of liquidation and reorganization;

order of the creditors and the liquidation of the

budget , etc.

Now is the time to say a few

words about a third of the form of incorporation of the

company:

2.3. Closed Joint-Stock Company This form of incorporation of the enterprise as a whole is

similar to the Limited Liability

Company. However, there are some differences. Closed joint-stock company is established

as a Limited Liability Company, one or several founders. But only the

corporation has the

right to issue shares, and these shares in the Closed Joint-Stock Company are distributed

among its founders. The number of shareholders in a Closed Joint-Stock Company shall not

be more than 50, or to carry out the transformation into a Public Company. The founders of

the agreement is

signed on the establishment, which expires after the private Limited

Liability Company and run by the founders of all their responsibilities to create it. In all

official documents before the name of the enterprise should

present the abbreviation

"ZAO." Responsibility, as well as for a Limited Liability Company - to the

value of the shares

of participants. The minimum capital - 10,000 rubles (≈ EUR 250).

Self-registering your costs will include:

state fee for registration of a company in the tax office (4000 rubles) (≈ EUR 120);

payment notarized signature on the application for registration of the company

(≈ 1,000 rubles) (≈ EUR 25);

payment of at least 50% of the share capital - not later than 3 months from the

date of registration of the tax office;

state duty for registration of the shares in the Federal Service for Financial

Markets (20,000 rubles) (≈ EUR 500)

A key advantage and

difference from the limited liability company is that to sell (give way,

etc.) their shares without

shareholder may notarization of the

transaction . The register of

13

shareholders

while the company may carry on their own.

Transfer of title to the shares

makes the head of the company (CEO). Another key advantage is that the shares are

transferred to the shareholder in the

trust , which allows you to not disclose the information

about the owner of the business. Otherwise, the Closed Joint-Stock Company is very similar

to a Limited Liability Company.

At present, in Russia there is a big law discussion about the elimination of such

organizational form as a Closed Joint-Stock Company, just for this reason. It is assumed that

there will only be a Public Joint-Stock Company.

The disadvantages of this organizational form:

any deal for the transition of ownership of shares (sale, donation, etc.) not be

notarized, which may provide an

opportunity for fraud;

requires registration of the shares in the Federal Service for Financial Markets

(apply for registration of shares needed for 1

month from the date of

registration, registration

deadline is 1 month);

significantly increases the amount of reporting on the shares of the Federal

Service for Financial Markets.

2.4. Company name Having determined the optimal organizational and form of incorporation, should seriously

consider the choice of company name. You can safely use your name or the

names of their

partners . It is desirable that the name of your company is not repeated the names of existing

businesses, but

during registration tax authorities cannot

refuse because of the coincidence

of names with other companies. This relates to the

field of copyright

protection .

You must use the official company name in official correspondence, invoices, receipts,

invoices, etc.

You must specify:

abbreviation of the legal form of the company (ZAO or OOO);

official corporate name;

the location address of the organization.

Try wherever possible, to use them to advertise your business. It should be noted that there

are some

items that cannot be used without permission. For example: the words “Bank”,

“Bank of Russia”, “Russia”, “Moscow”, “Insurance”, etc. For the use of

proper names of

cities, countries, etc., in the name of the company will be charged an additional fee. In

addition, the use of the

emblem of the country, the

republic , the city also requires a special

permit and payment.

14

In

conclusion , let's

compare some of the main parameters considered in this

chapter of

forms of incorporation of companies.

2.5. Comparison of different forms of incorporation of companies Private entrepreneur

There can only be a citizen of Russia.

The responsibility for liabilities - all its assets.

Accounting - accounting procedure for an individual entrepreneur is

easier :

income and expenditure and business transactions conducted by individual

entrepreneurs by fixing the “Book of income and expenditure and business

transactions”.

Taxes - taxation, depends on the tax system, there are some pros and cons for

both Private Entrepreneur and legal entities.

Discontinued operations - order the termination of an individual entrepreneur is

much easier to order liquidation of legal entities.

Registration - Registration deadline in tax office is 5 working days.

Limited Liability Company

The responsibility for liabilities - Limitation of Liability: You only lose their capital

contribution Accounting - Requires conducting official accounting and reporting in accordance

with the formal

requirements . The Company maintains records in accordance

with the requirements of the Federal Law "On Accounting" (from 21.11.1996 №

129-FZ).

Taxation - Taxation of, depends on the tax system, there are some pros and cons.

Discontinued operations - order of liquidation of a long and laborious.

Preparation of reports - Enough time-consuming procedure.

The authorized capital - The authorized capital of the company shall not be less

than 10,000 rubles (≈ EUR 250).

Any deal for the transition of ownership of the share capital (sale, donation, etc.)

must be notarized

Registration - Registration deadline in tax office is 5 working days.

Closed Joint-Stock Company The responsibility for liabilities - to the extent of the value of its shares.

Accounting - Requires conducting official accounting and reporting in accordance

with the formal requirements. The Company maintains records in accordance

15

with the requirements of the Federal Law "On Accounting" (from 21.11.1996 №

129-FZ).

Taxation - Taxation of, depends on the tax system, there are some pros and cons.

Discontinued operations - order of liquidation of long and laborious

Registration - Enough time-consuming procedure

Preparation of reports - Enough time-consuming procedure

Share Capital-The authorized capital of the company shall be not less than 10,000

rubles (≈ EUR 250).

Any deal for the transition of ownership of shares (sale, donation, etc.) not be

notarized.

Registration - Registration deadline in tax office is 5 working days.

Required state registration of the shares in the Federal Service for Financial

Markets (apply for registration of shares needed for 1 month from the date of

registration, registration deadline is 1 month)

In the first part of the lecture was

briefly considered some of the most popular to date forms

of incorporation of companies in Russia. Then in the second part of this lecture will provide a

brief overview of other existing Russian legal forms of companies.

16

3. TAXATION, DUTIES AND EXCISES 3.1. The essence of the tax system, the principles and functions of taxes The state, representing the interests of society in various cferah life, develops and

implements appropriate policies - economic, social, environmental, demographic, and

others. Through tax contributions generated financial resources of the state, accumulated in

its budget and

extra -budgetary funds. Taxation is

based on 15 social laws, the law on the

budget and the tax code.

Taxes - mandatory fees and charges levied by the state to individuals and businesses in the

budgets of the appropriate level or extra-budgetary funds at the rate established by law.

Payments are mandatory and free of

charge .

Taxes - a flexible

tool to influence which is in constant

motion economy: they help to

promote or constrain certain activities, to

guide the development of certain industries,

impact on economic activity of entrepreneurs, to

balance the effective

demand and supply,

to regulate the amount of money in circulation.

The tax system of the Russian Federation represented by:

•

collection of taxes, duties, fees and other charges levied in the established order in

the country;

• targeted payments to about 15 state budget funds;

• competent authorities in the field of taxation and the ways they interact with each

other;

• methods of calculating taxes, and tax control.

According to the

method of levying taxes are

direct and

indirect . Direct taxes are levied by

the state directly to the income and property taxpayers. The

subject of income tax

acts (

wages , profits,

interest , etc.) and the value of the property taxpayers (

land ,

fixed assets,

etc.). Indirect taxes are established in the form of surcharges to the

price of the goods or

service tariffs (excise, VAT and customs duties). These taxes are accrued to the enterprise so

that it

kept them from other taxpayers and donate the

Finance Ministry.

Depending on the

nature of betting distinguish regressive, proportionate and progressive

taxes.

Progressive tax - a tax that is increasing faster than income grows. For different sizes of

income set several scales of tax rates. Regressive tax is characterized by levying a

higher percentage of low-income and low percentage with higher incomes. This is a tax that grows

more slowly than income. Indirect taxes are often regressive.

17

Proportional tax - this is where a

single rate applies to income of any size. Proportional tax

may be regressive, if income derived from actual costs required to deduct

remain discretionary income that can

grow or

decrease after the introduction of new taxes.

Depending on the

authority , in order that emits certain taxes, federal and

local distinction.

There are federal taxes

base : income, profits and customs duties. The main type of local tax

is the property tax.

Taxes on their use are

divided into general and special. General taxes are intended to finance

current and capital expenditures of state and local budgets without any assignment to a

certain type of expenditure. Special taxes are earmarked. The legislation established that the

objects of taxation are:

profit ,

revenue , cost of certain goods, value-added

products , assets

of businesses and individuals, the transfer of property, separate transactions, certain types

of activities, the monthly minimum

wage , etc.

Taxes depending on the

sources of their coverage are grouped as follows:

1. taxes, the costs of which are

included in cost of goods (

works , services) - land tax,

insurance premiums;

2. taxes, the costs of which are included in net sales of products (works, services) - VAT,

excise duties,

export tariffs;

3. taxes, the costs of which are included in the financial result, income tax, property tax,

advertising , some targeted taxes;

4. taxes, the costs of which are covered by the profit

left at the disposal of enterprises -

the license fee for the right to trade, the collection of transactions executed on the

stock exchanges.

A method for implementing public use taxes as a tool of the cost of distribution and

redistribution of income expressed as a function of taxes.

The first and most consistently implemented tax function acts fiscal function, which

consists in the

formation of monetary income of the state of the state apparatus, the

army , the

development of

science and

technology , support for children, elderly and sick people, for the

cost of education, children's homes, healthcare, construction of public buildings, roads,

protection of the environment.

Another function of the tax - economic, which consists of exposure through taxes on social

reproduction, encouraging, restricting or

controlling the various processes. Benefits

encourage the development of that for which they are given, for example, if the

levy is not

part of the profit on the development of new technology, it encourages

technological progress, to

charity , to solve social problems. If you increase taxes on

excess profits, then

controlled by the

movement of the prices of goods and services. With the

growth of tax

18

revenues to the

treasury will decrease as proportion of entrepreneurs go bankrupt, will take

part in the

informal economy, incentives to work will fade.

The perfection of the tax system depends on the elasticity of demand and supply of goods or

services. Sellers

shift taxes on buyers when demand is inelastic. If the

proposal is inelastic,

then taxes are

passed on to the vendors. When tax rates are

reasonable , we

know their

purpose, their payment is usually not shy.

There are three ways to increase tax revenue: the expansion of the

circle of taxpayers, an

increase in the number of objects from which the tax is raised, raising tax rates. Tax rates

should be so high as to prevent inflation, but at the same time so low to stimulate capital

investment, to ensure the development of production.

Limiting the level of taxation is determined by the following criteria:

1. if the next increase of the tax rate revenues are

growing disproportionately

slow or

declining;

2. if the reduced rate of economic growth, reduced long-term capital investment,

deteriorating financial situation of the population;

3. the growing "shadow" economy, i.e. implicit or explicit tax evasion. The main

features of the tax system are summarized in Table 7.

In the tax system, there are a variety of benefits such as tax exemption for a number of

years , reducing tax rates, subtract the deductible

expenses , which the State concerned, the

establishment of discounts during the formation of different funds, the return of previously

paid taxes, tax credit or deferral of payments of taxes, exemption limit, the removal of

certain

elements of taxation, exemption of certain categories of taxpayers, etc.

In case of violation of tax legislation taxpayer liable to a penalty the

entire amount of the

concealed (undervalued) income or the amount of tax for a

hidden object of taxation, as well

as a fine of the same amount and interest at the rate of one three-hundredth of the

refinancing rate for each day of

delay . Repeated or deliberate concealment (determined by

the

court ) shall be

punished by a 2-and 5-

fold .

The Tax Code provides an evolutionary reform of the tax system, the establishment of the

level of taxes that taxpayers will be able to

survive , but it does not

hurt the budget. Should

be

provided with certainty, predictability and

transparency of the tax system. Corrects the

benefits are mostly only investment and social benefits. For small businesses, organizations,

retailers, and service

sector organizations, for all those who provide paid services for a

transition to a simplified system of taxation.

19

3.2. The main taxes In Russia, according to

claim 1 of Article 19 of the Law "On the basis of the tax system in the

Russian Federation" tax expense (income) of enterprises refers to federal taxes. Provided

that it is a regulatory budget sources, i.e. of the

incoming tax may be transferred to the

budgets of Russian

regions .

Payers of

income tax are enterprises - legal entities, their branches, foreign legal entities.

Subject to tax profits from the sale of goods (works, services), income from the sale of fixed

assets and other assets and income from non-operating transactions. Profit (loss) from sale

of goods (works, services) is defined as the difference

between the proceeds from the sale of

goods (works, services), value added tax and excise taxes and the cost of production and

sales, which is included in cost of goods (works, services).

Gains on securities of gaming, from

agency stand out from the gross profit and taxed at a

different rate. The

subjects of the Federation independently determine the tax rate. The

federal tax rate is 13% and the

maximum territorial law 22% (30% mediation).

Examples of

the benefits of income tax is a 100%

reduction in the amounts of income tax for public

organizations of disabled persons and specialized orthopedic companies, the application of

accelerated depreciation, which is a

condition for the provision of benefits to the

target using the money for the purchase of fixed assets. Tax incentives should not

reduce the

amount of tax calculated without the

benefit of more than 50%. Income taxes paid in Russia

has

advanced . Significant benefits for income tax are small businesses. The newly created

small enterprises first two years do not pay income tax, if engaged in the production and

processing of agricultural products, farm goods,

building materials, medicines,

housing construction, including repairs, provided the proceeds from this activity 70%, third year 25%,

4 years 50% (90% of revenues). At the termination of the tax

returns and increases the

percentage of the Central Bank.

Value Added Tax (VAT) - an indirect tax on goods and services, which has an input tax paid

to suppliers and output accrued on its own

turnover . In the taxable turnover is

almost everything: the cost of goods

sold , services, financial assistance from other companies, funds

received from fines, penalties penalties, advances on export enterprise

losses , barter

transactions, interest for the provision of money on credit. When calculating the taxable

turnover of goods, which are charged with excise taxes, customs duties, it includes the

amount of excise and customs duties.

The current legislation establishes a list of turns, not subject to VAT, as well as a list of

products, goods, works and services that are exempt from the imposition of this tax. These

revolutions, in particular, the goods (works, services) produced and sold medical-

industrial workshops in psychiatric and neuropsychiatric

institutions , non-governmental organizations

for the disabled. VAT payers are legal entities and individuals (end-payers). Do not pay the

20

tax individuals engaged in

entrepreneurial activities without forming a legal entity (before

the tax code).

Currently, the VAT rate set as follows: 10% on food (except for excisable goods) goods,

goods for children on the list approved by the Government of the Russian Federation, and

20% for other goods (works, services), including excise foodstuffs. On 01.01.1997 in the

Russian Federation introduced the method of invoicing, which governs the

process of

registration of the settlement documents for goods, works and services, so that is not

enough to allocate tax, we

still have a tax invoice.

The amount of VAT to be a contribution to the budget, calculated as the difference between

the amount of tax received from customers for sold them goods (works, services), and the

amount of tax paid to suppliers.

Excise tax - Indirect taxes included in the price of goods. Excise duties levied on these

products (products) ethyl alcohol of all kinds of raw materials, alcohol,

wine , drinking

alcohol, vodka, liquor, cognac, champagne, wine, natural, other alcoholic beverages,

beer ,

tobacco, jewelry, motor gasoline, cars . Rates of excise on excisable goods shall be the same

throughout the Russian Federation and are provided as annexes to the law.

Amount of excise duty to be a contribution to the budget, calculated as the difference

between the amount of excise tax, which is calculated on taxable turnover excise taxes, and

the amount of excise tax paid to suppliers for excise goods. Crediting mechanism introduced

by the Law on excises. For example, if the purchase of alcohol excise tax paid, and the

alcohol used in the production of non-excise products (medicines), the amount of excise

duty shall be compensated from the budget.

Property tax - In accordance with the instructions of the tax inspectorate of the Russian

Federation are subject to taxation,

plant and

equipment , intangible assets, inventories and

expenses on the balance of the paying company. Fixed assets, intangible assets, low value

items for tax

purposes are recorded at net book value.

For tax purposes is determined by the

average annual value of the property business.

This cost for the reporting period is determined by dividing by 4 the amount obtained from

the addition of half the value of the property on

January 1 of the year and the first day of the

following month of the reporting period and the amount of value of the property on the first

of every month all the other quarters of the reporting period. The maximum amount of the

tax rate on the assets of the enterprise may not exceed 2% of the tax base, and by the

decision of the local government, this percentage can be set to a smaller size.

Property tax businesses to financial

results . Payers of income tax are individuals as having

and not having a permanent

place of residence in the Russian Federation. The object of

taxation from the citizens is the total income earned in a

calendar year, either in cash or in

kind (salaries, bonuses, fees,

dividends , profit distribution, gifts, tickets, food, subscription,

21

payment for children in

child care centers, etc. .). The

composition of the total income of

citizens also include the amount of material and social benefits provided by companies to

their employees personally and the amount of material

gain on borrowings and deposits in

banks. In a combined annual income does not include all types of pensions paid under the

pension legislation of the Russian Federation, severance pay, paid severance, compensation,

employee benefits paid to them within the rules (

travel , field allowances, the use of private

vehicles for official purposes).

Individuals whose income for the year did not exceed 5,000 rubles taxable amount is

reduced by the amount of income equivalent to twice the

statutory minimum wage and the

same amount for the children and dependents of each month. When combined income

reaches 5000rubley and 1 penny to 20000rubley benefits are determined in the amount of a

single statutory minimum wage. The table given the

scale of income tax on the taxable gross

income received in a calendar year. Income tax exemptions are given for housing once in a

lifetime for a period not exceeding three years 5000 minimum wage.

An example of local taxes can be land tax. The object of land tax are land granted to legal

persons and citizens. Land tax is calculated based on the area of land that is taxed and

approved by the local authorities, land tax rates based on the normative price of land in

rubles per hectare.

Tax on advertising - One of the most significant in terms of volume of incoming payments of

local taxes is a tax on advertising. Payers of the ads are the advertisers. The tax rate for

advertising is up to 5% of the cost of advertising works and services from the advertiser.

Other examples of local taxes are local taxes from transactions made on the stock

exchanges, the fees for the right to trade, landing fees to

Police and other such purposes.

In conclusion it should be mentioned that recently a very important issue for

entrepreneurs is the abolition of the single tax (ENVD - Ediniy Nalog na Vmenenniy Dohod),

when it will be and how it will be replaced. Cancel ENVD

really planned in the

near future.

Since it was

reported that the Ministry of Finance of the existing solutions that are making

fundamental changes in the activities of the business sector of the Russian economy.

However, it is in the

plans to cancel the

flat tax only for certain categories of entrepreneurs,

and for the

rest - in the long term.

3.3. Tax rates in 2013 in Russia This text is a short, simplified certificate at the rates of the main taxes in

force in Russia in

2013. For

perfect accuracy , it should go directly to the texts of the laws on taxes and fees. It

should be borne in mind that it is extremely important not only to a particular tax rate, but

also the object of taxation, to which this rate applies.

22

VAT rate: VAT rate - 18%. It is used most often.

The VAT rate on certain groups of goods - 10%

VAT rate - 0%, mainly export, trade precious

metals ,

space , more precisely, see sub-

paragraphs 1 through 10 of Article 164 of the Tax Code of the Russian Federation

In certain instances, the so-called settlement rates:

derivative of the VAT rate 10% - calculated as (10 / (100 +10)) * 100%

derivative of VAT at 18% - calculated as (18 / (100 + 18)) * 100%

These VAT rate effective from the 1st of January 2009.

The income tax rate:

Since January 1, 2009 effective basic rate of income tax - 20%. Of which 2% to the federal

budget, and 18% is credited to the budgets of subjects of the Russian Federation.

In addition to the basic rate of income tax set so-called special rates:

income tax rates for certain types of

bond : 0%, 9%, 15%

The size of the tax rate of income tax on income received in the form of dividends -

0%, 9%, 15%

The size of the income tax rate for foreign companies, the income is not related to

the activities in the Russian Federation through permanent - 10%, 20%

The income tax rate for the CBR 0%

The tax rate on personal income: The basic rate of income tax in 2013 - 13%.

Suitable for any income, except those for which special rates of personal income tax - 9%,

15%, 30%, 35%

Personal income tax rate 35% applies to:

A. the proceeds of the cost of prizes and

awards , exceeding the amount of the

B. income from interest on deposits in banks in excess of the specified dimensions

C. the amount of interest savings for the taxpayer receives

loan (credit) funds in excess

of the specified dimensions

Personal income tax rate of 30% is imposed on:

Income received by individuals who are not tax residents of the Russian Federation, except

for income received as dividends from equity participation in the activities of Russian

companies

15% personal income tax rate applies to:

23

Income received by individuals who are not tax residents of the Russian Federation, in the

form of dividends from equity participation in the activities of Russian organizations

9% personal income tax rate is applied to:

A. Income from equity participation in the activities of organizations received in the

form of dividends, individuals who are tax residents of the Russian Federation

B. The interest income on mortgage-backed bonds, issued before January 1, 2007, and

the income of the trustor mortgage obtained on the basis of acquisition of mortgage

participation certificates issued by the mortgage to manage January 1st , 2007.

Tax rates for the use of special tax regimes:

1. Rate

ESHN (Ediniy Selskohozjastvenniy Nalog) (unified agricultural tax) - 6%

2. Rate ENVD (Ediniy Nalog na Vmenenniy Dohod) (single tax on imputed income) -

15% of the imputed income

3. Rate USNO (Uproschennaja Sisteme NalogoOblozhenija) (simplified taxation

system)with the object of taxation revenue (simplified taxation system) -6%

4. Rate USNO (Uproschennaja Sisteme NalogoOblozhenija) (simplified taxation

system) with the object of taxation revenue minus expenses - 15%

However, the laws of the Russian Federation can be differentiated rates are set by the USNO

(Uproschennaja Sisteme NalogoOblozhenija) (income minus expenses), in sizes from 5 to

15%.

24

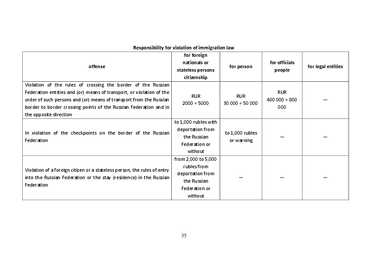

4. LABOUR RELATIONS (INCLUDING IMMIGRATION LAWS) 4.1. Entry and stay of foreign citizens in the Russian Federation Traditionally, Russian law divides the foreign nationals residing in the territory of the Russian

Federation into two categories, arriving in the order, which requires a visa and arriving in the

visa-free regime. For each category of foreign nationals

running its own procedure for

processing the documents.

The period of temporary stay of foreign citizens in the Russian Federation is limited:

•

validity of visas for citizens entering Russia visa regime;

• 90 days for citizens entering Russia visa-free (except for foreign nationals who have

permission to work).

Foreign citizens for which a visa is necessary to

remember that:

A. the purpose of his

visit to Russia must match the type of visa

B.

continuous stay of foreign citizens in the Russian Federation on the basis of a

multiple of annual business visa cannot exceed 90 days out of every 180 days

Every foreign national who

comes to the territory of the Russian Federation is obliged to fill

in a migration card, issued to him at the border. A completed entry part of the migration

card is

withdrawn officials customs control, and completed an

exit part - is a foreign citizen.

When leaving the Russian migration card is dealt at passport control.

In order to legally stay in the territory of the Russian Federation a foreign citizen must have

the following documents:

valid passport;

valid visa (entry visa, if available);

migration card;

notice of the migration registration (tear-off coupon);

work permit (if the purpose of the visit to Russia - employment).

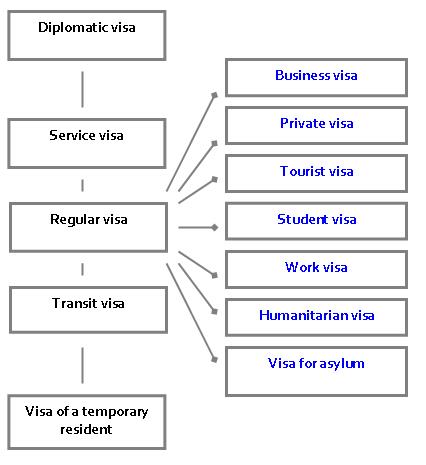

4.2. Types of visas for foreign citizens in the Russian Federation Depending on the purpose of his visit to the Russian Federation a foreign citizen is issued a

Russian visa. Russian visa may be single,

double and multiple.

Single-entry Russian visa allows a foreign citizen to

cross the state border of the Russian

Federation once on entry and once on departure from the Russian Federation.

Double-entry Russian visa allows a foreign citizen for double entry into the Russian

Federation.

25

A multiple-entry Russian visa allows a foreign citizen the right to a multiple (more than two

times) to enter the Russian Federation.

Federal Law of the Russian Federation

dated August 15, 1996 № 114-FZ "On the

Procedure for Exit from the Russian Federation and Entry into the Russian Federation,"

identifies the following visas:

Diplomatic visas are issued based on the decision of the Ministry of Foreign Affairs of the

Russian Federation, with a circulation (

Note Verbale) of the Ministry of Foreign Affairs, the

diplomatic or consular

mission of a foreign state, an international organization or a

representative office in Russia for foreign citizens who have diplomatic status.

Business visa is issued based on the decision of the Ministry of Foreign Affairs of the Russian

Federation, with a circulation (Note Verbale) of the Ministry of Foreign Affairs, the

diplomatic or consular mission of a foreign state, an international organization or a

representative office in Russia for foreign citizens who have official status.

Ordinary visa depending on the purpose of the visit of a foreign citizen can be private,

business,

tourist , educational,

labor , humanitarian, to enter the Russian Federation in order

to obtain

asylum .

An ordinary private visa is issued for a period of up to 3 months, foreign nationals

who enter the Russian Federation with a guest visit to an

invitation issued at the

request of the citizens of the Russian Federation, foreign citizens with a residence

26

permit in the Russian Federation, or a legal entity. In addition, the visa can be

issued in

connection with the need for

emergency treatment or due to serious

illness or

death of a close relative. The visa may be single or double.

Ordinary business visa can be single or double for a period of up to 3 months, or a

multiple of up to 1 year. Continuous residence on the basis of a multiple business

visa issued by one year cannot exceed 90 days out of every 180 days. The visa is

issued on the basis of an invitation to enter the Russian Federation, issued by the

inviting party. The visa is issued to foreign nationals who enter the territory of the

Russian Federation for the purpose of negotiations, presentations, to address

specific business issues: the conclusion and

renewal of contracts, commercial

services, and participation in conferences, symposia, congresses and other events,

bearing trade and economic nature, to

improve training and retraining; drivers of

vehicles carrying out

regular passenger and freight services,

crew members of

aircraft and ships, for medical examination and treatment, adoption; lectures at

colleges and professional

schools , and for the time reporters and technical

staff of

foreign media representatives. In addition, on the basis of ordinary business visa

enter foreign nationals deported to the Russian Federation from the territory of

foreign states, in accordance with agreements on readmission.

An ordinary tourist visa is issued to foreign nationals for up to 1 month, entering

the territory of the Russian Federation as a tourist, on the basis of a contract for

the provision of tourist services (travel

voucher ), and confirmation of receipt of the

organization, the

tour operator . The visa can be single and double, individual and

group.

An ordinary training visa is issued to foreign nationals who enter the territory of the

Russian Federation for training in educational institutions. The visa is issued for a

period of up to 3 months, with the possibility of extending continuously for the

duration of the agreement on education concluded in accordance with the laws of

the Russian Federation, but not more than 1-n for each subsequent year visa.

Ordinary work visa is issued to the diplomatic mission or consular office of the

Russian Federation, foreign citizens entering the territory of the Russian Federation

in order to work on the basis of an invitation from the organization, which is an

employer or customer service. Ordinary work visa is issued for a period of 3 months

with the possibility of

further extending continuously for the territorial

body of the

federal

executive body in charge of migration, the duration of the employment

contract or a civil contract, but not more than 1 year for each subsequent visa.

Work visa is issued for a highly qualified professional for the duration of the work

permit, which is valid

until 3 years on the basis of a labor contract.

27

Humanitarian visa is issued to foreign nationals who enter the territory of the

Russian Federation for

scientific , cultural,

political , sporting or

religious ties and

contacts, pilgrimage and charity or humanitarian aid. The visa can be single or

double for a period of up to 3 months, or a multiple of up to 1 year. Continuous

residence on the basis of a multiple business visa issued by one year cannot exceed

90 days out of every 180 days. The visa is issued on the basis of an invitation to

enter the Russian Federation, issued by the inviting party.

An ordinary visa to enter to the Russian Federation in order to obtain asylum issued

to a foreign citizen for a period of up to 3 months based on the decision of the

Ministry of

Internal Affairs of the Russian Federation on the recognition of refugee

status of a citizen in the Russian Federation. This visa can only be a single.

A

transit visa is issued to a foreign citizen for transit through the territory of the Russian

Federation or to the evacuation of a foreign citizen who has

arrived in order to require a visa

(for

passengers of cruise ships, citizens of countries with which there is an agreement on

visa-free entry, and passengers who commit visa-free transit to 24

hours ). The visa is issued

for up to 10 days. If the foreign national must be through Russian territory by air, the visa is

issued for a term of not more than 3 days. If a foreign citizen who

goes through the territory

of the Russian Federation in the country of destination for passenger cars, a visa is issued for

the period necessary for travel by the shortest route, calculated on the basis of daily

vehicle travel of 500 km. Visa code TP1 can be only once, and with the code TP2 single or double. A

transit visa is issued only if all required, in accordance with the legislation of the Russian

Federation, the supporting documentation.

Temporary residence visa is issued to foreign citizens with temporary residence permit at

the place of authorized residence. Temporary residence visa is issued for a period of 4

months of a foreign citizen who is

allowed to enter the territory of the Russian Federation

for temporary accommodation with an

option to

extend it by issuing multiple-entry visas for

the duration of the temporary residence permit. A foreign national who has received a

temporary residence permit in the period of temporary stay in the territory of the Russian

Federation issued a multiple-entry visa temporary residence for the duration of the

temporary residence permit.

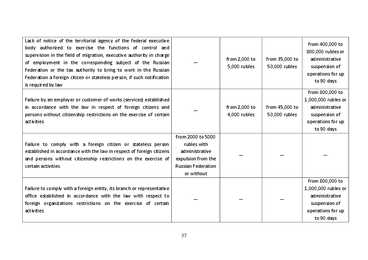

4.3. Migration Registration of Foreign Citizens in the Russian Federation In accordance with the Federal Law "On Migration Registration of Foreign Citizens and

Stateless Persons in the Russian Federation" temporarily staying in the Russian Federation a

foreign citizen must stand on immigration registration after seven working days from the

date of arrival at the place of stay. For migration registration, a foreign national upon arrival

at the place of sojourn, the receiving side photocopy of your passport with a valid visa (for

visa entry to the territory of the Russian Federation) and the migration card. The receiving

28

party applies to the bodies authorized to carry out registration of foreign citizens in the place

of stay (offices of the Federal Migration Service of Russia and the post office), with the

notice, and then passes the detachable part of the Notification foreigner. Note in the

detachable part of the Notification (humps) in the form of a stamp is a confirmation of the

migration registration.

Removal of foreign citizens with migration control, i.e. fixation of this fact in the public

information system of migration control by

organs FMS automatically in the following

cases :

When setting the foreign citizen registered as migrants in their new place of

residence; - when leaving a foreign citizen of the Russian Federation (data

transferred from border control);

as well as some of the other cases provided by law.

That

means that the receiving side above the duty is removed.

In cases where a foreign national to stay in hotels, lodges, spas, etc. migration registration is

carried out in the administration of the

hotel during the day.

Specific details of migration control for the highly skilled

specialist (hereinafter – “VKS” –

“Visoko Kvalificirovanniy Specialist”), as well as members of their

families :

1. VKS, as well as their family members are exempt from the need to migration

authorities provided the entry and stay in the territory of the Russian Federation up

to 90 calendar days;

2. If the

length of stay VKS, as well as his family members is more than 90 days, you

must carry out the procedure of the migration registration within 7 working days

after the 90-day period;

3. VKS and members of their families are exempt from the need of migration

registration when

moving to a new place of residence in the territory of the Russian

Federation, provided that they have the current migration registration and their

location in the new location less than 30 days;

4. If the length of stay in the new location will be more than 30 days, the migration

registration must be made within 7 working days after the 30-day period.

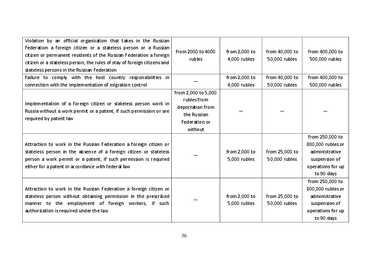

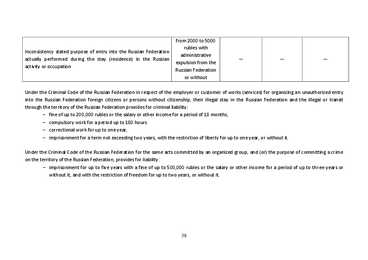

The procedure to get the work permits for foreign citizens arriving in Russia in the visa:

In order to work a foreign national entering the territory of the Russian Federation in the

visa, the employer must make the following documents:

1)

Permit for invite a foreign labor Permission to

hire foreign workers is valid for one year within the quota, which is

approved annually by the Government. Permission to

attract indicate information such as

the number of employees, their positions, citizenship, and the territory or territories to

which the document.

29

It should be noted that

prior to the

submission of documents for the issue of a permit to hire

foreign workers must complete the quota, i.e.

filing applications for quota by 1 May for the

coming year, and a month before going to the immigration authorities to file a civil service

employment information on the requirements for employees.

2)

A work permit The work permit is issued for one year under a permit to hire foreign labor.

3)

Notice of solicitation for employment of the foreign national. At the conclusion of an employment contract or a civil contract with a foreign national

entering the territory of the Russian Federation in the visa, the employer shall within ten

days notify the local tax authority.

4)

Accreditation for the visa and registration support. Accreditation for the visa and registration service gives companies the right to invite

foreign citizens, ie issue invitations to the business and work visas.

5)

Work visa Your work visa consists of two phases:

issuance of the invitation for a single work visa valid for three months;

remap single work visa to multiple work visa for a period not more than a year.

6)

Notice of the migration registration (tear-off coupon). 4.3.1. The procedure for bringing the work of highly skilled professionals (VKS) VKS recognizes a foreign national who has

experience , skills and achievements in a particular

field of activity, if the

conditions to attract him to work in the Russian Federation

involve receiving their salaries (wages)

1) in an amount not less than one million rubles at the rate of one year (365 days) - for highly

skilled professionals who are scientists or teachers, in their invitation to engage in research

or teaching activities of the state-accredited institutions of higher education, public

Academies of Sciences or their regional offices, national research centers or public research

centers;

2) without

taking into account the size requirements for wages - for foreign citizens

participating in the

project "Skolkovo" in accordance with the Federal Law "On the

innovation center" Skolkovo ";

3) in the amount of not less than two million rubles at the rate of one year (365 days) - for

other foreign nationals.

30

NB! Foreign nationals may not be required to work in the Russian Federation as a highly

skilled

occupation for preaching or other religious activities, including the commission of

worship and other religious rites and ceremonies, religious instruction and religious

education of the followers of any

religion .

Features of the application of the legislation on highly qualified professionals:

A. Employers may be the only VKS:

Russian commercial organizations;

Russian scientific organizations, educational institutions, professional education

(with the exception of vocational religious education (religious educational

institutions);

health agencies, and other organizations engaged in research, scientific-technical

and innovation activity, experimental development,

testing , and training in

accordance with national

priority areas of science, technology and

engineering of

the Russian Federation, if they have in the cases provided by law the Russian

Federation, the State of accreditation;

duly accredited in the Russian Federation, branches of foreign legal entities.

and not subject to administrative punishment for violation of foreign labor for 2

years from the time the motion of calling for VKS.

B. To attract VKS should observe the following conditions:

in the payment of wages in the amount provided by law;

VKS and his family should be provided with voluntary health insurance from the

time of entry into the Russian Federation shall have the right or on the basis of the

contractual arrangements entered into by the employer or customer of works

(services) from a medical institution to receive

primary health care and specialized

care.

C. Features:

The work permit is issued for a term of employment contract, but not more than 3

years. Period of validity of the work permit may be repeatedly extended for the